Author: Andrew Tang, Graphics: Nina Tagliabue

The BRB Bottomline

The Biden Administration recently passed a $1.9 trillion stimulus package that includes a $1,400 stimulus check for those that qualify. For many Americans, this financial support can alleviate many short-term concerns. Read this article to find out how you should allocate this money and what other Cal students are doing!

The Situation

Though it may feel like we have gotten past a huge hurdle with the high efficacy and rollout of vaccines, many still endure economic setbacks resulting from the pandemic. The Biden Administration recently passed a $1.9 trillion stimulus package that would provide crucial relief to millions of Americans in hopes of negating some of these problems.

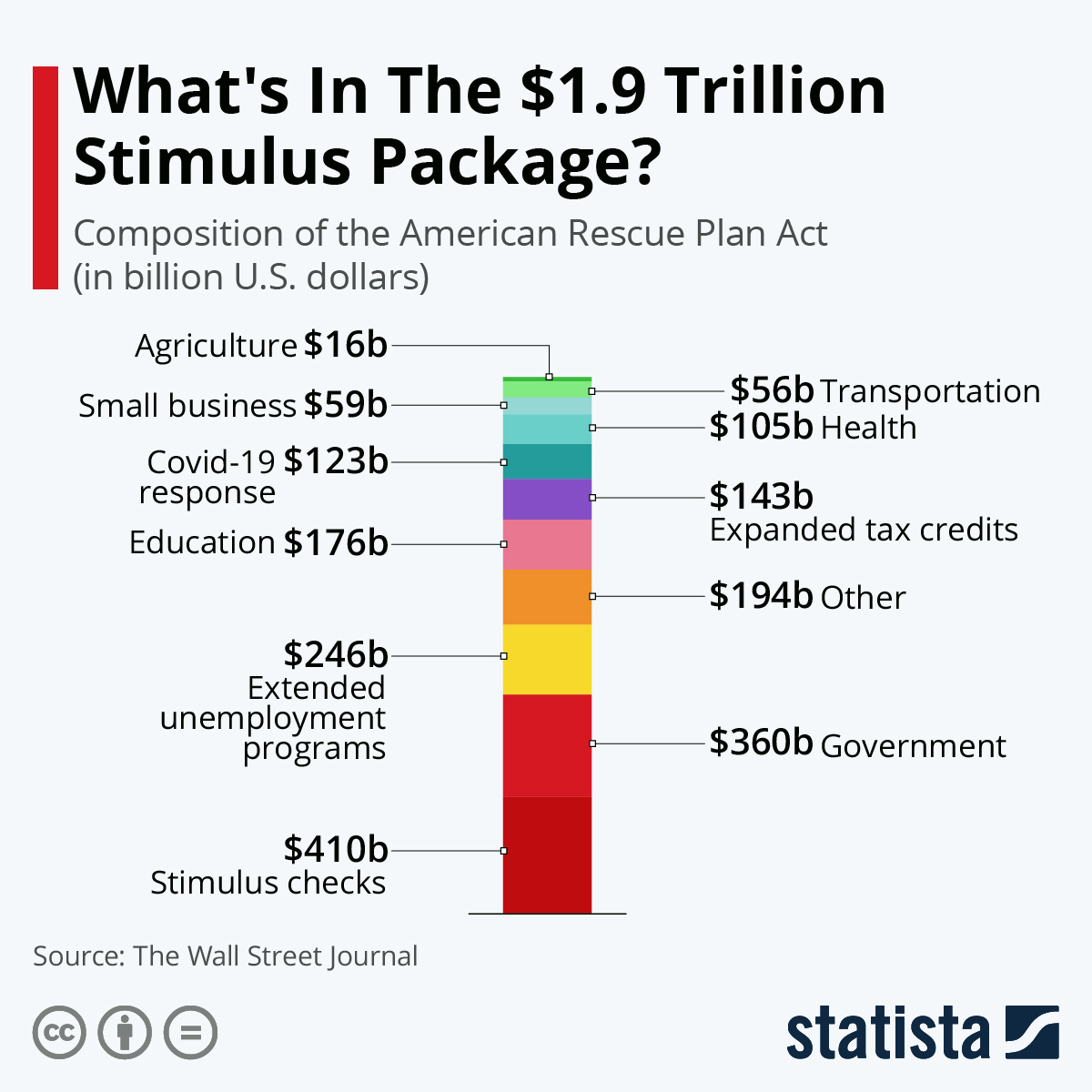

As part of one of the largest relief bills since the Great Depression, over $400 billion was dedicated to direct payments for American taxpayers. Individuals making no more than $80,000, single parents earning less than $120,000, and couples with household incomes of up to $160,000 are all qualified for a $1,400 check. These checks are not taxable and are considered a refundable tax credit by the IRS. Hundreds of billions were allocated to state and local governments, along with the education sector and Covid-19 response. Maybe most important of all, $300 weekly federal unemployment payments were extended till September 6th.

Not only are the stimulus checks designed to support those in financial need, but it also serves to keep money flow stable between borrowers and lenders. Though this injection of cash can serve as a short-term solution, it does not guarantee any future stability. This most recent stimulus check comes after $600 and $1,200 checks from December and the Cares Act, respectively, that were sent to x amount of Americans. The Fed can only print a certain amount of money without exceeding steady rates, and future taxpayers will end up with the burden of repaying these debts.

Figure 1: Statista

How to Spend Your Stimulus

As Cal students, a majority of us or our immediate families will receive a stimulus check. A Federal Reserve survey last October found that there was a close-to-even distribution in how Americans spent their stimulus checks, including spending the money, saving it, and paying off debts. Thus, it’s imperative that we understand the different ways to utilize this money, depending on your individual or household circumstances.

To simplify the decision-making process, I’ve created a flow chart, categorizing individuals into five different subsets. With input from Bears for Financial Success peer educator, Shreyas Hariharan, here’s my advice:

- Pay off bills

For those students that are living paycheck to paycheck and barely scraping by, your main and only priority should be to cover your basic needs. Some bills that would fall under this category range anywhere from weekly groceries to internet bills. Though a stimulus check may not seem like a large amount, it can provide some much-needed breathing room for millions of families. Shreyas suggests working on a monthly budget to help monitor spending. Here’s a template that Bears for Financial Success created!

2. Cover any existing debts

A rule of thumb is to start with paying off debts with the highest interest rates. For example, if you had mortgages, student loans, and credit card debt, you would want to clear the credit card debt first. It seems like a no-brainer, but debts can quickly accumulate, so make sure you get this done. One popular route is refinancing to decrease interest rates on your current loans. Refinancing are a great option due to historically low interest rates, while your stimulus check could put a large dent in closing costs.

3. Start saving or investing

If you’re able to complete the previous tasks, consider adding this money to a savings account. This could come in the form of starting or accumulating an emergency fund. It’s common practice to allocate at least 20% of your income to savings. A rainy-day fund can prove crucial if unanticipated medical bills, job loss, or repairs occur. Set aside enough to live off of for a few months and be sure to only use the emergency fund when you absolutely need something. Ideally, one should look to accumulate anywhere from $2,000 to $5,000 in emergency funds. Shreyas recommends that college students should also make it a priority to invest in funds to set up long-term stability.

4. Treat yourself

There’s absolutely nothing wrong with rewarding yourself every once in a while for being financially responsible. Maybe there’s a pair of shoes you’ve always wanted or it’s time to upgrade to a new phone. Be mindful of not biting off more than you can chew but also enjoy your successes. Celebrating small wins can go a long way in improving your happiness and productivity.

5. Give back to those in need

For those that can afford to forgo the extra cash, look to pay it forward. Whether it means helping out a struggling friend or donating to a shelter, your efforts will certainly be appreciated. Giving back leads to lasting happiness, so seriously consider this opportunity if you’re lucky to be in this position. Further, certain charitable contributions can qualify for deductions in adjusted gross income, producing another reason to give back.

Student Spending

Although I created a five-step process to utilize your stimulus checks wisely, the American Rescue Plan Act passed a few months ago, meaning that many have already allocated this money towards certain needs. Therefore in an effort to understand how these direct payments were spent, I reached out to fellow Cal students, and here’s what they had to say.

Jimmy Lee (3rd Year): “With everything that’s occurred over the past year, this round of stimulus checks was much needed for many Americans. Fortunately, I didn’t have an immediate need for the money, so I had to think carefully about where I wanted to put it. After talking with some friends, I decided that the wisest thing to do was to put $400 into my savings account for emergency use. I ended up contributing the remainder into my Roth IRA.”

As you can see, there are a wide variety of ways that Americans can spend their stimulus checks, depending on their financial situation.

What Now?

Though the stimulus checks have come at a crucial time, they can only do so much as the ramifications of the pandemic are still being felt.

This sentiment has been shared throughout Congress, with Senator Ed Markey of Massachusetts stating that this recent check is “only a downpayment” to be followed up with recurring payments. Currently, 74 congressional lawmakers are in support of a 4th payment. Further, a recent analysis by the Tax Policy Center at the Urban Institute found that an additional $1,400 payment would bring 7.2 million Americans out of poverty. Recently, California Gov. Gavin Newsom announced that residents under the $75,000 annual income limit would be eligible for an additional $600 payment.

There is no doubt that further stimulus packages would greatly improve the financial situation for millions of Americans. However, these moves would be faced with considerable opposition, and we’ll need to wait a while before any potential aid comes through. Don’t rely on stimulus checks to bail you out of bad situations. With or without another stimulus, the five-step process still applies and is sure to streamline your budgeting.

I hope this helped answer any questions you might’ve had. If you’re interested in everything surrounding stimulus checks, feel free to reach out and we can go deeper into the topic!