So Much Changes Every Week, But Not Our Fed Call.

Authors: Andrés Larios, Sydney Sibrian, Faith Spalding

Editors: Venus Dhanda, Sydney Sibrian, Faith Spalding

Intro:

Welcome to the Weekly BluRB, a newsletter catered to students and professionals to get the latest news and insights on global markets. Get prepared for the week by reading four weekly stories circulating around equity markets, macro trends, geopolitics, and new business developments. And the best part: we’ll give you an informed view about where we think prices, policy, and trends are going in the near future. The content in these writings is for informational purposes only and does not constitute financial or investing advice.

Equity Markets: S&P < 6000 – Rate Cutting Path & Trump’s Cabinet Picks Hinder Stock Market Rally

The S&P 6000 is no more, but we’re confident it will be back by the end of the year. Amid growing uncertainty around interest rates and upcoming policy changes, major indexes faced declines this past week. The S&P 500 dropped by 2.3% this past week, the Dow Jones dropped by 1.39%, and the tech-heavy Nasdaq Composite fell by 3.49%. Trump’s cabinet picks did little to reassure investors of future market stability. In our US Macro section, we explain why equity investors are correct in being skeptical about a December rate cut, however, we don’t believe this should deter investors until Trump takes office.

The Russell 2000 Index, our preferred gauge for SMID-cap stocks, slid nearly 4.5% last week following interest rate guidance news. As noted in last week’s edition, SMID-caps are particularly sensitive to rate changes. The increasing probability of a constant target Fed Funds rate going into 2025 will slow the broadening out in growth that we have been expecting to see in the stock market. Despite this, we remain bullish on small and mid-cap stocks, but recognize it will be a bumpy path to broadening out, especially if interest rate cuts are muted.

Last week, we recommended financials, tech, and energy stocks as the best way to position oneself for the Trump presidency. A month ago, we analyzed the financial sector’s third quarter earnings, emphasizing how their guidance and growth signaled strong prospects for a soft landing. Today, financials yield the most growth potential, with its S&P sector index growing by half a percentage point in the past week, despite market-wide downturns. Mike Wilson, CIO and Chief US Equity Strategist at Morgan Stanley echoed our sentiment from last week’s BluRB, stating that “The more important call is not the index, it’s being in the right parts of the market.”

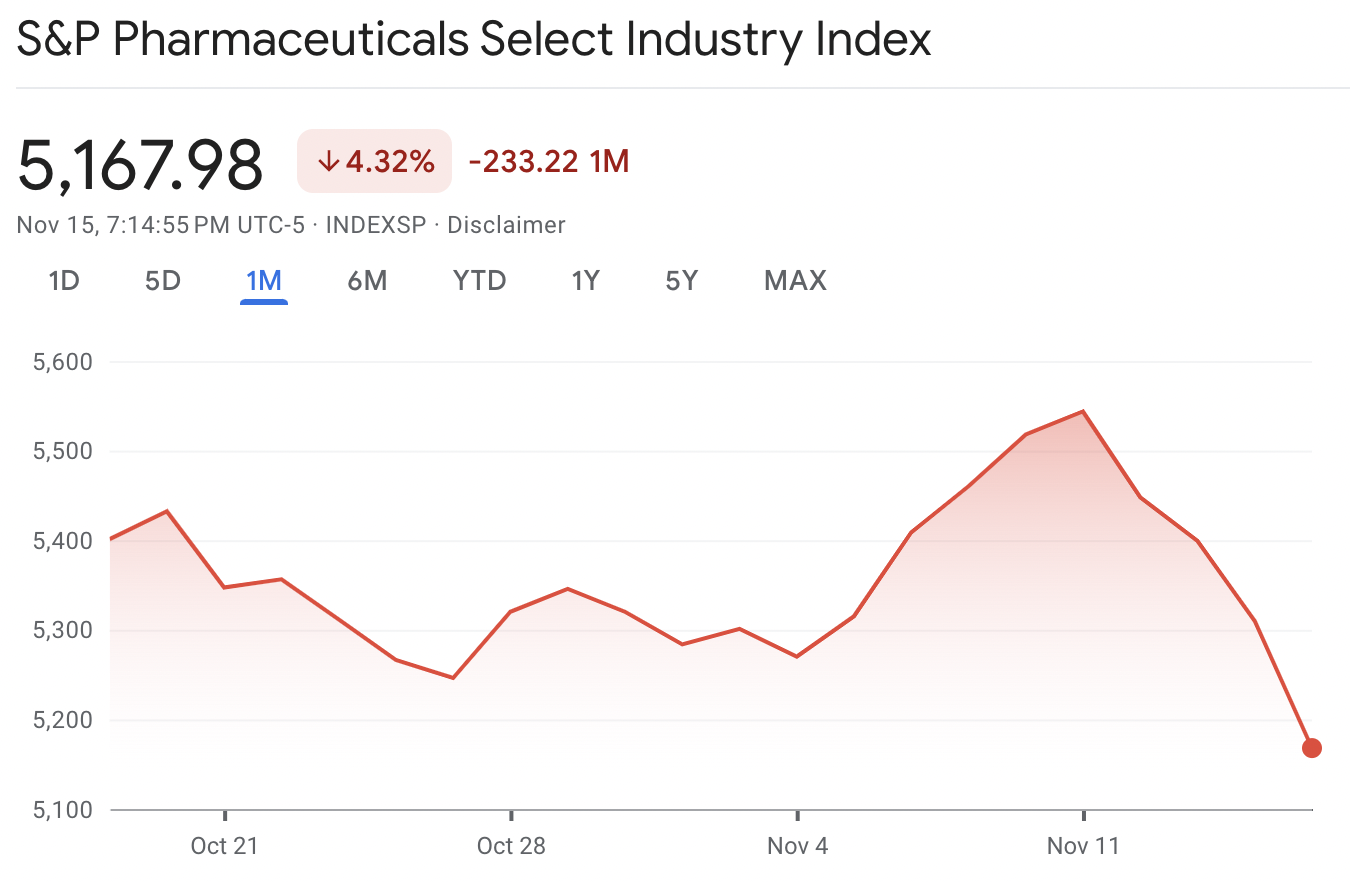

President-elect Trump’s cabinet picks contributed to this week’s index declines. Most notably, Trump plans to nominate Robert Kennedy Jr. for the position of Head of The Department of Health and Human Services. RFK Jr., known for his controversial stances on vaccinations, pesticides, and processed foods, sent pharmaceutical stocks tumbling this past week, with the S&P’s Pharmaceuticals index dropping 6.34%. If confirmed, Kennedy is poised to play a more significant role in Trump’s cabinet than initially anticipated following November 5th’s presidential outcome. We expect increased regulation in the broader health industry and project that its growth will lag behind the overall index, if RFK Jr.’s appointment passes through Congress.

Chart 1: Following RFK Jr.’s Nomination Pharmaceutical Stocks Dip

How many times have we ~almost~ recommended buying Nvidia but not pulled the trigger? Too many. Today we’re finally doing it. In sync with market trends, Nvidia fell 3% as of Friday’s close. This minor dip has negligible importance considering Nvidia’s staggering $3.483 trillion market cap. As a key supplier for high-end GPU’s essential for AI operations, Nvidia has become virtually indispensable, cornering the industry. The company’s supply of next-gen GPUs are already sold out for the next 12 months, with demand still on the rise. Overall, the stock continues its sharp upward trend, rising more than 186% this year alone. It remains comfortably in the buy zone. With Nvidia’s earnings report set to release later this week, analysts expect an 81% jump in revenue and 85% jump in share earnings. The firm’s impressive growth fundamentals coupled with its role in AI innovation, make Nvidia a compelling long-term investment. Investors (and us) remain bullish, anticipating continued performance momentum.

US Macro: Our December Call is Admittedly Normative… But We’re Using a Lot of Charts to Explain Why We’re Right

This past week provided more clarity on the upcoming December Fed meeting, as several key data points dropped, including the NFIB Optimism Survey, CPI, PPI, and Jobless Claims. On Thursday, Catherine Rampell of The Washington Post interviewed Fed Chair Jerome Powell, and President of the Minneapolis Fed, Neel Kashkari spoke to Bloomberg. Both offered fresh insights into the Federal Reserve’s rate cutting plans. Given this new economic data and verbage to analyze, we are maintaining our call for no rate cut at December’s FOMC meeting. Here’s why.

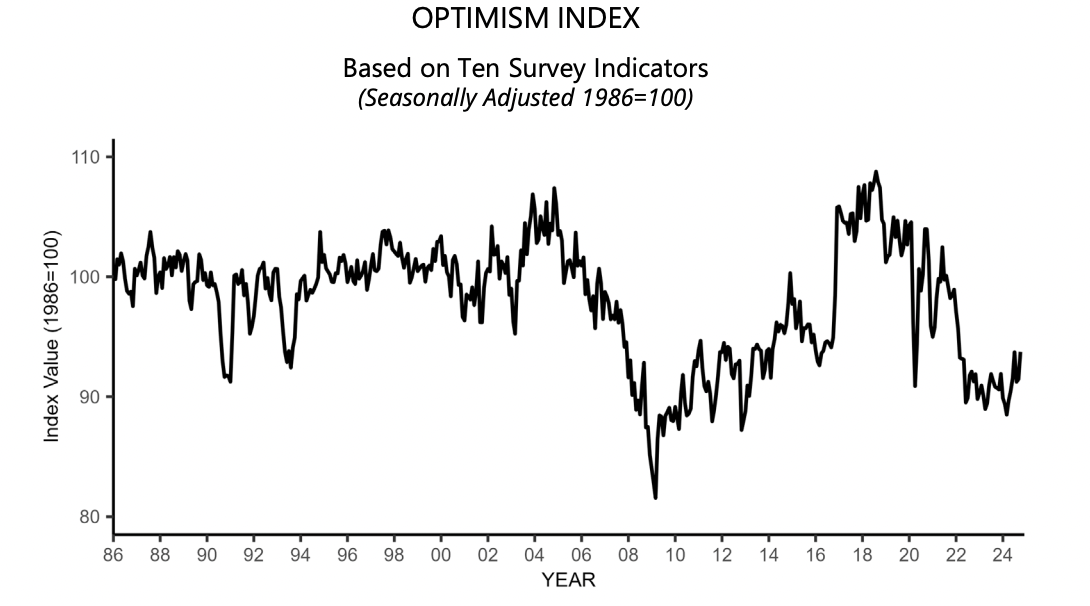

The National Federation of Independent Business’ (NFIB) monthly Small Business Optimism Index drew our attention for two main reasons. First, their optimism index, which aggregates responses from 10 survey questions, inched up to 93.7 (base 100), a 2.2-point increase from September. While this suggests that main street’s sentiment is improving, the index remains below its historical average of 98, signaling cautious optimism. We note that the S&P 500 has grown by roughly 56% in the past two years, yet small business owners have remained largely pessimistic about the economy (Chart 2).

Chart 2: NFIB Optimism Index Shows Small Businesses are Cautiously Optimist

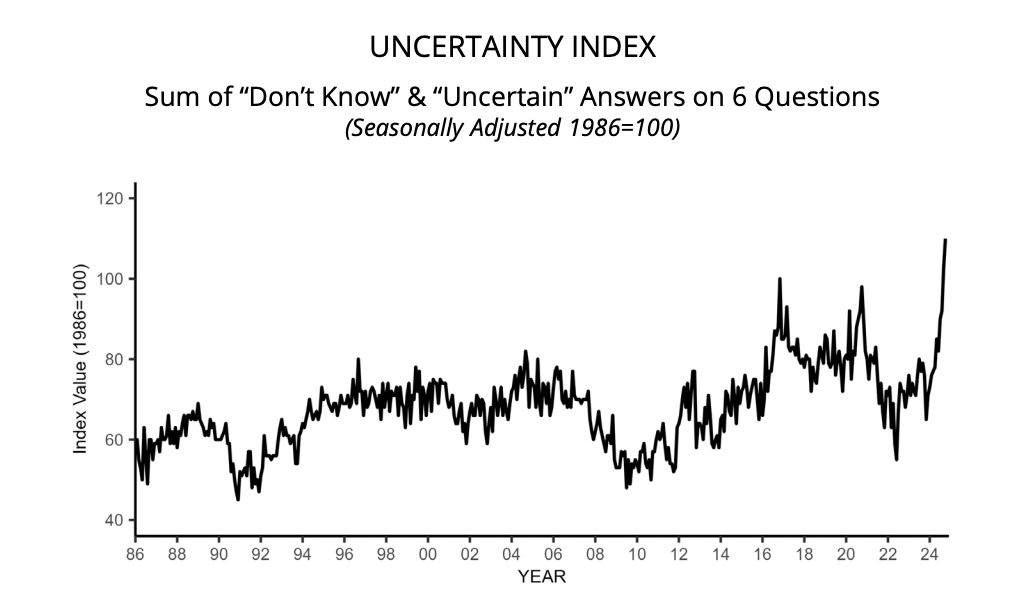

The NFIB’s Uncertainty Index (Chart 3) highlights lingering concerns among small businesses over issues such as presidential outcomes, Trump’s inflationary fiscal policies, and the increasing reliance on debt to finance an increasing amount of government spending. NFIB Chief Economist, William Dunkelberg states, “The economy cannot continue to finance its growth by borrowing more money.” According to the report, uncertainty levels should drop significantly next month, barring any abnormal shocks.

Chart 3: Uncertainty Index Reaches All Time High in October

Inflation remains the top concern for small business owners, with higher input and labor costs outpacing concerns over taxes, poor sales, and quality of labor. In October, the industries where price hikes were most frequent were finance, retail, construction, and services, reflecting a good mix between durable and non-durable goods. Notably, a net positive 26% of small business owners surveyed reported planning to raise prices (1 percentage point higher than the previous month), and we expect price levels to rise further due to seasonal spending trends as the Holiday season approaches. This survey reaffirms our hawkish stance on inflation.

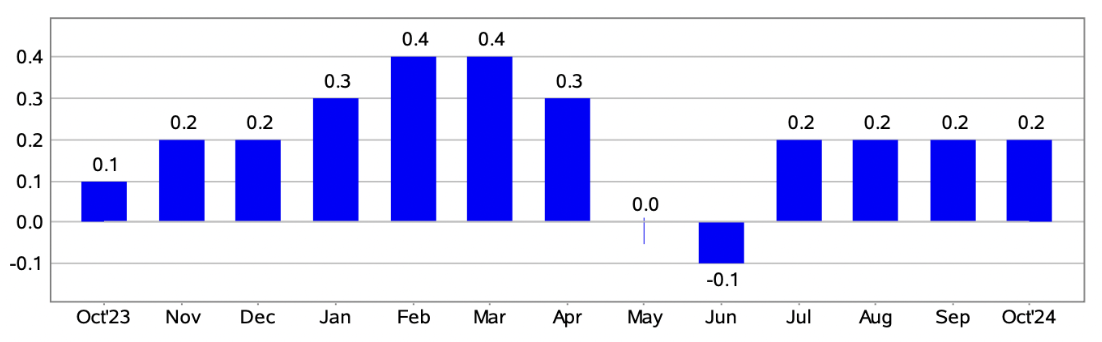

What does the actual inflation data tell us? Consumer prices have risen by 0.2 percent for the last four months; however, a closer analysis reveals inflation grew from 0.179% in September, to 0.244% in October, suggesting that Chart 4 may be somewhat misleading. This figure aligns with Wall Street analyst’s expectations, which is supportive of expectations for a December rate cut. That said, this data point continues to support our view.

Chart 4: One Month Percent Change in CPI (Seasonally Adjusted)

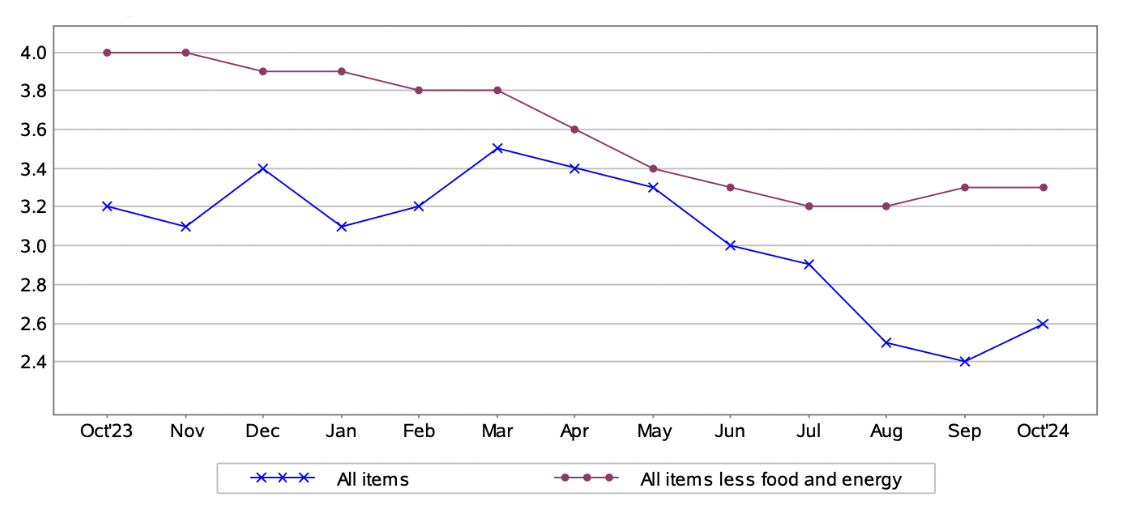

Chart 5 tracks the 12-month percent change in Consumer Price Index (CPI). When focusing on ‘all items less food and energy’, inflation remains at 3.3% year-over-year, a level that warrants skepticism regarding the Fed’s battle against inflation. While food and energy prices are volatile and driven by international factors, they are essential components of daily consumption. Looking at our chart below, it’s clear that food and energy prices are reducing inflation (2.6% all items vs. 3.3% all items less food and energy), so what durable goods are keeping prices sticky?

The short answer is shelter. In the CPI, the Bureau of Labor Statistics (BLS) measures the prices of shelter using real and implied (the implicit rent a homeowner would pay if they were renting) rent prices. This is a lagging indicator because lease agreements change over years, and instead are subject to long term trends. The index for shelter rose 0.4% in October, accounting for more than half of inflationary pressures. Excluding shelter, year over year inflation rate sits at 1.3%. This bodes well for the Fed, reflecting progress towards their soft landing goal. It has also led investors to believe that a 25 basis point rate cut in December is in order, but we remain skeptical.

Chart 5: Twelve Month Percent Change in CPI (not seasonally adjusted)

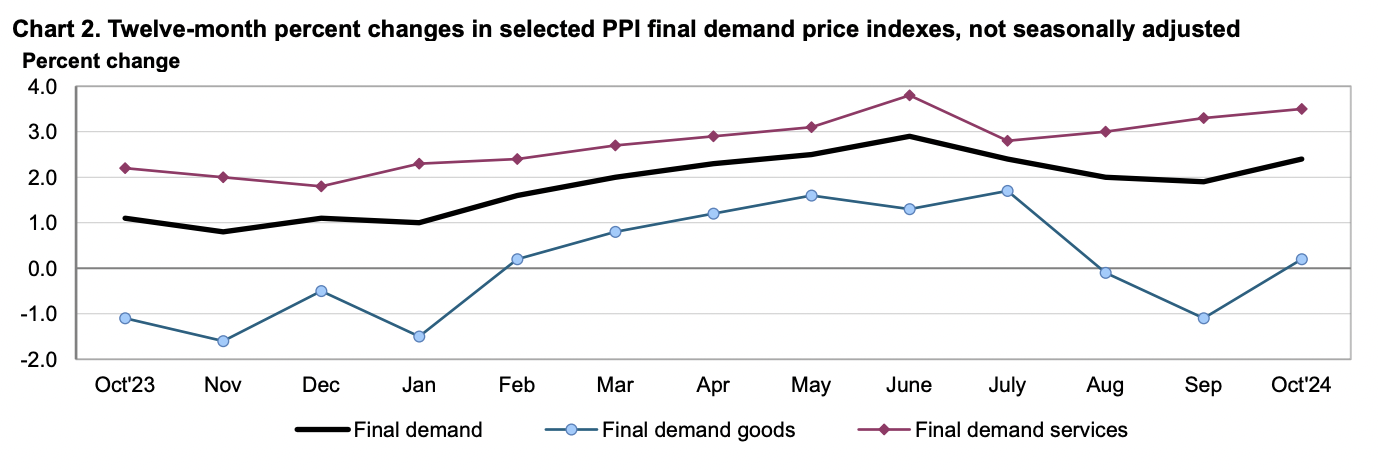

Our skepticism is reinforced by the latest PPI report (also released this week and produced by the BLS). In this report, we see that final demand services are driving supply-side inflation, by a lot. We also see that October is the first reading since July where final demand goods inflation increased. Final demand prices increased by 0.2% over the past month, and 2.4% over the past year, with the inflation reading also increasing for the first time since June. This is in line with the NFIB Optimism Index findings that we elaborate on above. Inflation is still hitting corporations, and hence disinflation is slowing at a faster rate than expected 75 basis points cut later.

Chart 6: Twelve Month Percent Change in PPI (not seasonally adjusted)

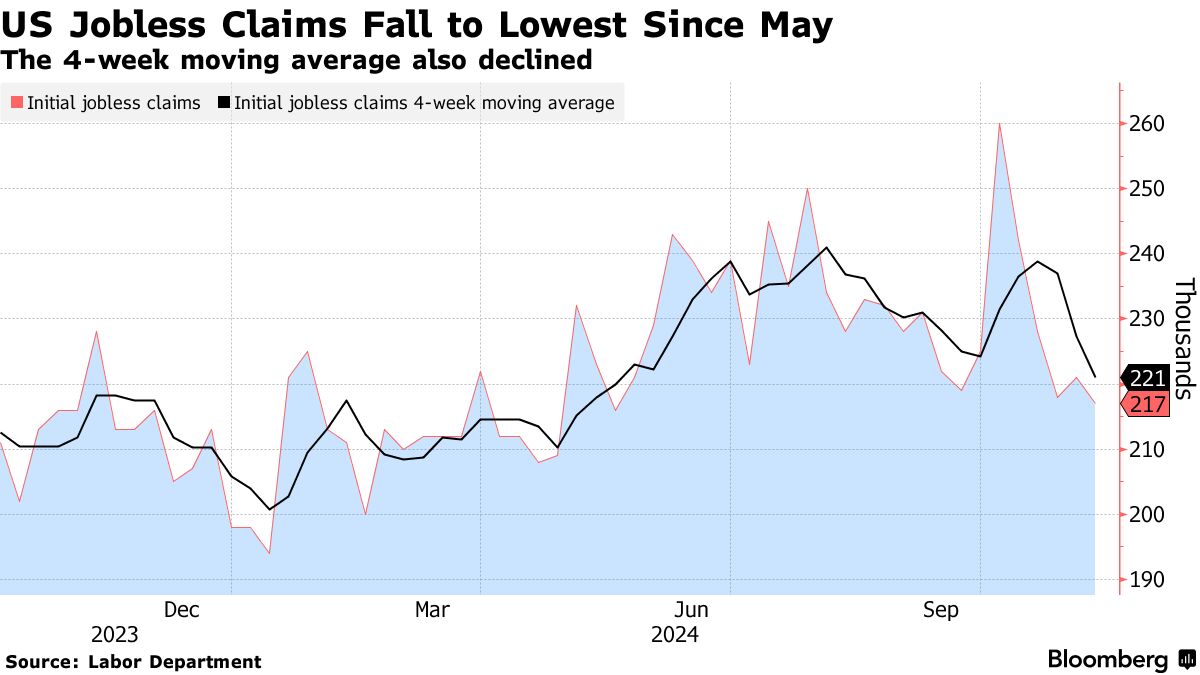

On Thursday, Minneapolis Fed President, Neel Kashkari told Bloomberg, “I’ve been surprised at the resilience of the U.S. economy in the face of seemingly quite high policy rates. Yet the labor market has stayed strong, and the economic growth continues to surprise us.” This statement, made before the PPI report release, but after the CPI report release, solidifies our December stance. There is ample evidence of U.S. consumer resilience ‘saving’ the economy after COVID-19, leading to high inflation and the sharp increase in interest rates. The same can be said today. We are still in a (relatively) high interest rate environment, and the economy is booming. With jobless claims falling this week (Chart 7), we believe the strength of the labor market and the U.S. consumer is going to continue exacerbating the Fed’s inflation troubles.

Chart 7: U.S. Jobless Claims and 4-Week Moving Average Decline Showing Economic Resilience

On Thursday, Fed Chair Jerome Powell spoke in Dallas.

We know that reducing policy restraint too quickly could hinder progress on inflation. At the same time, reducing policy restraint too slowly could unduly weaken economic activity and employment. We’re moving policy over time to a more normal setting but the path for getting there is not preset.

Here, Chair Powell acknowledges the progress the Federal Reserve has made in calming inflation to a point where they can now focus equally on stable prices and maximum employment. At the same time, he highlights how the path to R-star is uncertain. We believe his acknowledgement of ‘inflation first’ highlights his policy priorities and supports our view.

The economy is not sending any signals that we need to be in a hurry to lower rates. The strength we’re seeing in the economy gives us the ability to approach our decisions carefully.

This statement can be perceived in two ways. The first aligns with our call for no rate cut in December. The economy’s strength and resilience in a high interest rate environment is evidence enough of a need to slow the rate cutting cycle. This, coupled with uncertainty regarding President-elect Trump’s economic policies, places the Federal Reserve in a good position to begin 2025 at a closer-to-neutral rate than initially anticipated before the election. The second perception is: cut rates now since we’re already not expecting many cuts during Trump’s presidency.

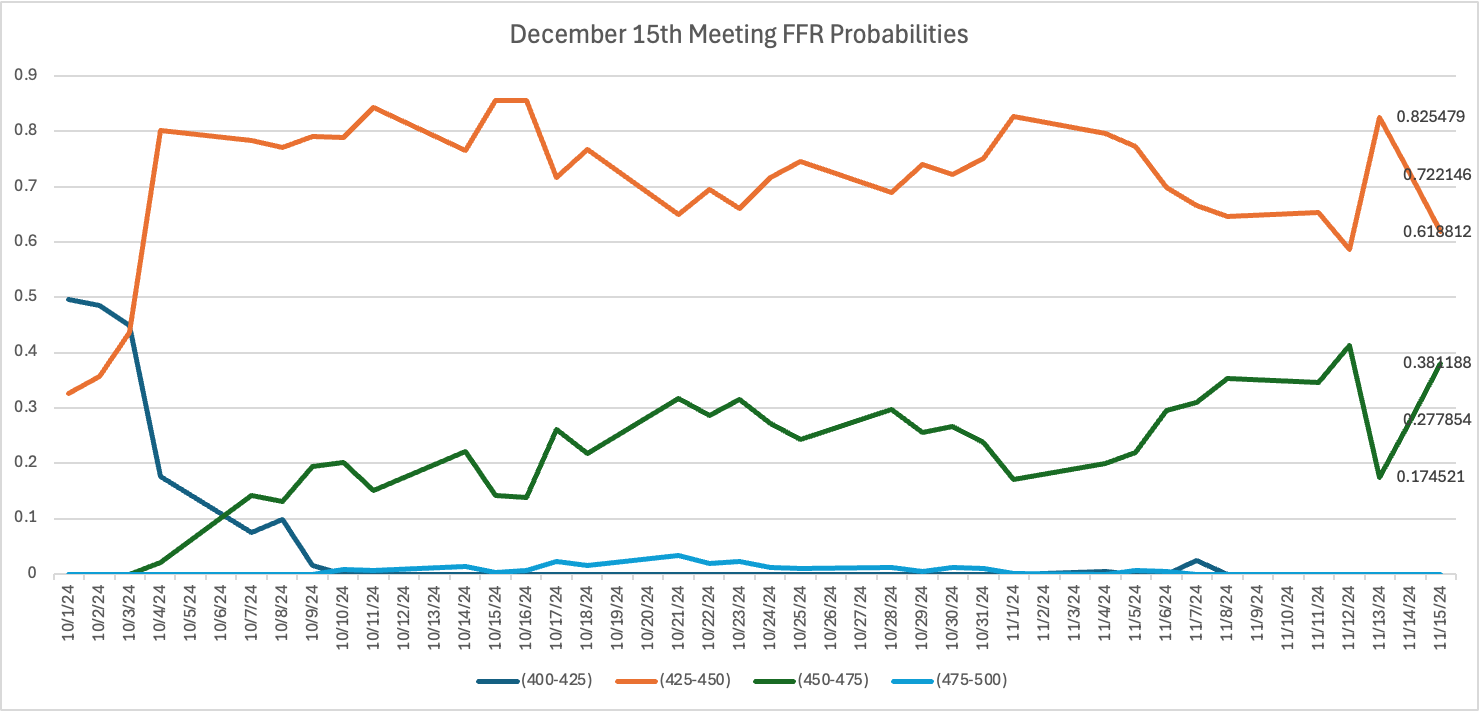

But this argument is dovish for speculative reasons, and coupled with our interpretations of the data above, completely discount the uncertainty that main street is facing, the uptick in supply-side costs, and the unrelenting strength of the U.S. economy in terms of productivity and employment. In our view, there is no point in cutting just because you can. The Fed is not behind the yield curve at the moment, and it would be dangerous to try to get ahead of the yield curve. Chart 8 shows that although our current stance is the less likely outcome today, after this week’s data drops showing inflation data largely in line with consensus, the probability of a rate cut remains roughly unchanged from the beginning of the week. This points to our call being more likely than what is currently priced-in.

Chart 8: Time Series of December 15th Fed Meeting Rate Probabilities

Global Macro: Emerging Markets and Trump: Major Dub or Major L?

Global markets continue to respond to the re-election of former U.S. President Donald Trump, with the S&P, Nasdaq and Bitcoin seeing massive post election gains. But even while U.S. markets experienced initial gains, as election enthusiasm subsides, we have to focus our attention on global emerging markets. Global markets are still trying to figure out what a Trump presidency means, especially because emerging market local currencies bore the brunt of Trump’s 2016 election win.

India:

India is among the countries that could potentially benefit from Trump’s policies, especially when considering his threat of 60% tariffs on all Chinese imports. Due to India’s impressive economic growth, minimal reliance on Chinese and U.S. consumer markets, and a focus on maintaining currency stability, we expect an increased attractiveness of the country amidst global unease. Compared to its slower 2016 growth rate, India’s shift to a sturdy yearly GDP pace of 8.2% (as of March 2024) reveals its recent economic successes. According to Carl Vermassen at Vontobel, Indian government bonds represent an “attractive” diversification while the central bank’s FX policy of stabilization makes the rupee one of the best risk-adjusted carry trades. However it’s important to remain on the lookout, as Indian equity valuations remain high, and the rupee hit a record low on November 6th post-election, despite a fairly quick recovery.

Mexico:

Market apprehension in Mexico was less pronounced than after Trump’s first election in 2016, with the Peso experiencing a 3.6% drop last week as opposed to the Peso’s 8% drop in 2016. However, BRB’s recent article highlights Mexican GDP growth’s deceleration and the USD/Peso exchange rate’s two-year low. Despite a quick recovery, this indicates a shaky economic environment for Mexico amidst Trump’s policy proposals of closing the border, mass deportations and increased tariffs.

Ukraine:

Ukraine faces uncertainty under a new Trump Presidency. While Ukrainian bonds experienced post-election boosts with the prospects of the Russo-Ukrainian war ending, threats of U.S. aid withdrawal from Ukraine could cause major spillover into European markets if peace talks fail. European Union member states have spent more than $175 billion on aid to Ukraine since the start of the war in February 2022, and that could increase dramatically. Trump’s unpredictability and relationship with Putin may dampen Ukrainian territory conversations, but he continues to stand behind his pledge to end the “unwinnable war”.

What Works and What Doesn’t Work?

As election momentum subsides, the realities of a second Trump Presidency are setting in, and emerging markets must be ready to face a wave of unpredictability. As U.S. markets experienced initial post-election gains, we believe India is best positioned to profit from Trump hardline trade policies. Our most attractive EM is India because of its lower-risk position between U.S. and Chinese markets, good currency valuation, and strong bonds. Given Indian Prime Minister Modi and President-elect Trump’s friendship, India’s counter-weight position against China may pay to its geopolitical advantage.

This same sentiment doesn’t necessarily extend to countries like Mexico; already experiencing economic turbulence and GDP growth deceleration, Trump’s policies may exacerbate an already tedious situation. As far as Ukraine goes, although Ukrainian bonds experienced post-election gains, Trump’s proximity to Putin may lead to roadblocks in engineering major peace solutions. The risks associated with the geopolitical situation outweigh the potential gains.