Author: Sean O’Connell, Graphics: Lydia Qu

THE BRB BOTTOMLINE:

This article explores how countries became indebted before and during COVID-19 and whether the current strategy of sovereign debt reduction is an effective way to stabilize countries in the midst of a public health crisis.

The last nine months of the pandemic have deeply damaged the domestic economy and humbled a spirit of steady growth many Americans were hoping to enjoy into the 2020s. However, while the coronavirus marks a severe setback in US economic well-being, in many other nations COVID-19 is pushing tenuous financial situations beyond the brink. Faced with mounting external public debt and uprooted export supply chains, many of the world’s most impoverished countries have been forced into fiscal insolvency and government standstill.

What happens when entire countries can no longer pay their debts in the 21st century? Is the international economy strong enough to handle dozens of insolvent countries—especially in the middle of a global pandemic? This article explores how countries became indebted before and during COVID-19 and whether the current strategy of sovereign debt reduction is an effective way to stabilize countries in the midst of a public health crisis.

Endemic Debt in a Pre-Pandemic World

For anyone familiar with organizations like the World Bank and IMF, learning that a severe debt crisis in developing countries is a regular occurrence comes as no surprise. A report by Brookings estimated that developing nations would have around $1 trillion in debt service due this year on long-term loan repayments. The World Bank further found the debt-to-GDP ratio in developing countries has grown from 114 to 168 percent over the last ten years. However, these metrics might seem inconsequential when considering that the US paid $522 billion in debt interest payments this past year and has a 136 percent debt-to-GDP ratio. Other wealthy counterparts like Japan also have debt ratios as high as 200 percent.

Unfortunately for impoverished nations, holding debt often generates more debt. Most developing countries are not considered “stable” borrowers by international lending banks and private investors for a variety of reasons, from internal conflict to agricultural overreliance. Credit rating agencies therefore often penalize high debt developing countries by assigning them poor credit ratings that lock them out from receiving competitive lending offers. As a result, one of the few ways lenders have to analyze whether a country will repay its loans is to look at sovereign debt levels..Consequently, countries already suffering from high debt levels are often unable to borrow their way out, even wealthy nations accrue staggering debt tolls with little consequence. Arvind Subramanian, India’s former chief economist, told the Economist in 2017 that the rating agency’s policies were akin to “closing the stable doors after the horses bolted.”

Finding Financial Lifelines

So, what do you do when your FICO score is too low for the bank to consider lending to you? If you’re a country, international lenders are your best bet. For some high and middle-income nations, this means the International Monetary Fund (IMF): a consortium of wealthy lenders who provide large-scale fiscal relief to countries they believe will repay their loans.

For most low and middle-income states, the World Bank Group is the more natural choice. The World Bank is half a financial agency, half a nonprofit group. It makes money by lending to middle-income countries at regular market (LIBOR) rates and uses the proceeds and sovereign donations to provide low-interest rates to low-income countries. These low-interest investments are provided by the International Development Agency (IDA)—an organization that provides assistance to 74 lower and lower-middle-income countries around the world.

The Bank committed $30.48 billion through IDA last fiscal year towards financial restructuring, health and social programs, disaster relief, and development programs. Most importantly for indebted countries, IDA and the IMF jointly manage two major debt relief initiatives for heavily indebted countries: The Heavily Indebted Poor Country Initiative (HIPC) and Multilateral Debt Relief Initiative (MDRI). HIPC was developed in 1996 to help 39 of the world’s poorest countries gain access to development loans at concessional levels while restructuring and paying down their debt. The MDRI, by contrast, helps middle-income countries still struggling with debt problems after completing the HIPC Initiative by providing relief for loans from a variety of additional multilateral banks. The MDRI and HIPC combined have provided $100 billion debt relief since the mid-1990s.

Health Crisis and Freefall

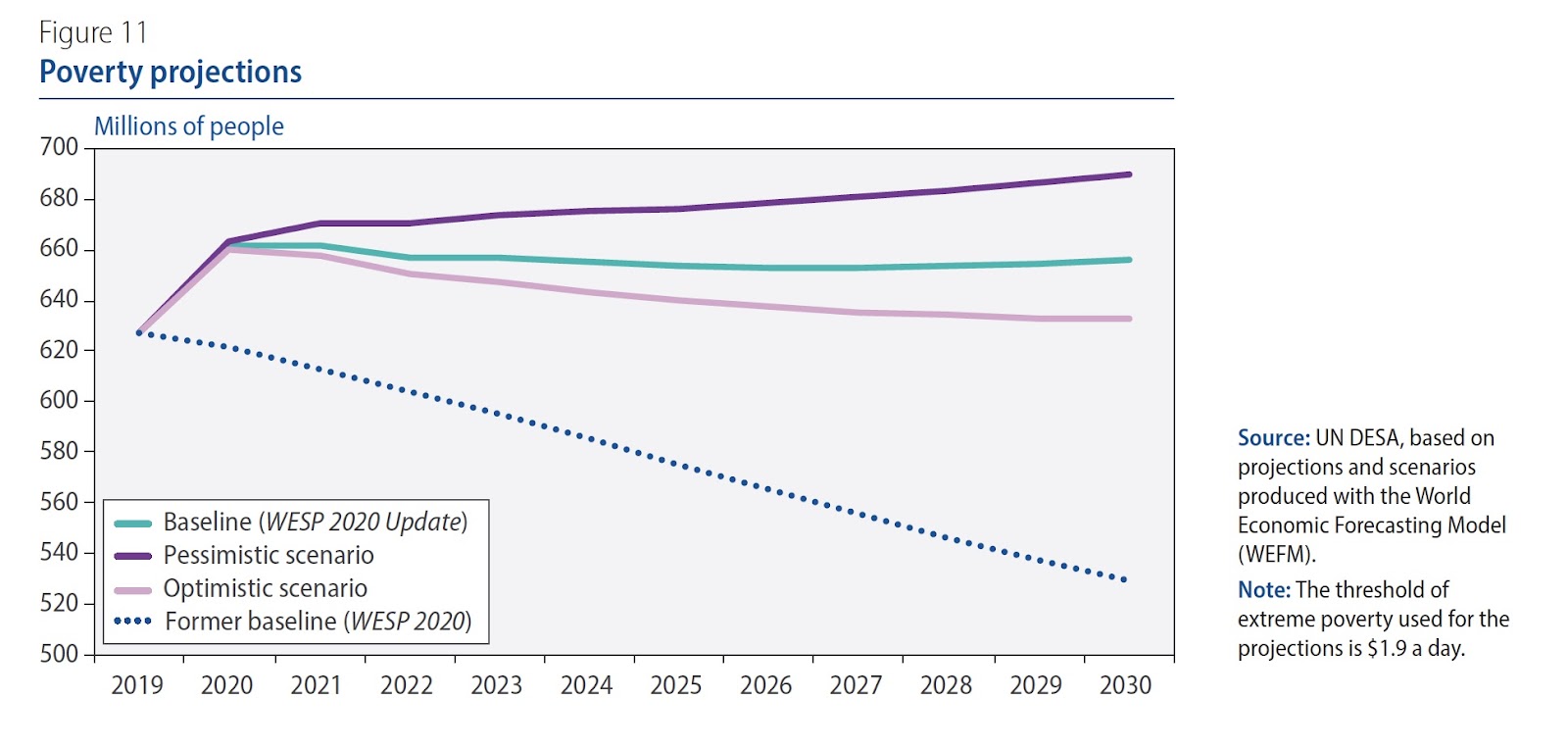

Though debt default was never an easy thing for countries to face, the coronavirus has greatly increased the risk of default for many countries while simultaneously reducing the amount of international financing available to insolvent borrowers. The scale of the problem is not lost on the world’s largest humanitarian organizations: the United Nations predicts that a debt crisis in the world’s poorest countries will likely force governments to cut spending on social programs that could push upwards of 140 million individuals back into extreme poverty. Exacerbating this problem is the $130 billion outstanding funding required by low and middle-income countries to service their sovereign debt payments this year. A report by the Centre for Economic Policy and Research called requiring these payments in the midst of the coronavirus “tantamount to squeezing water out of a stone.”

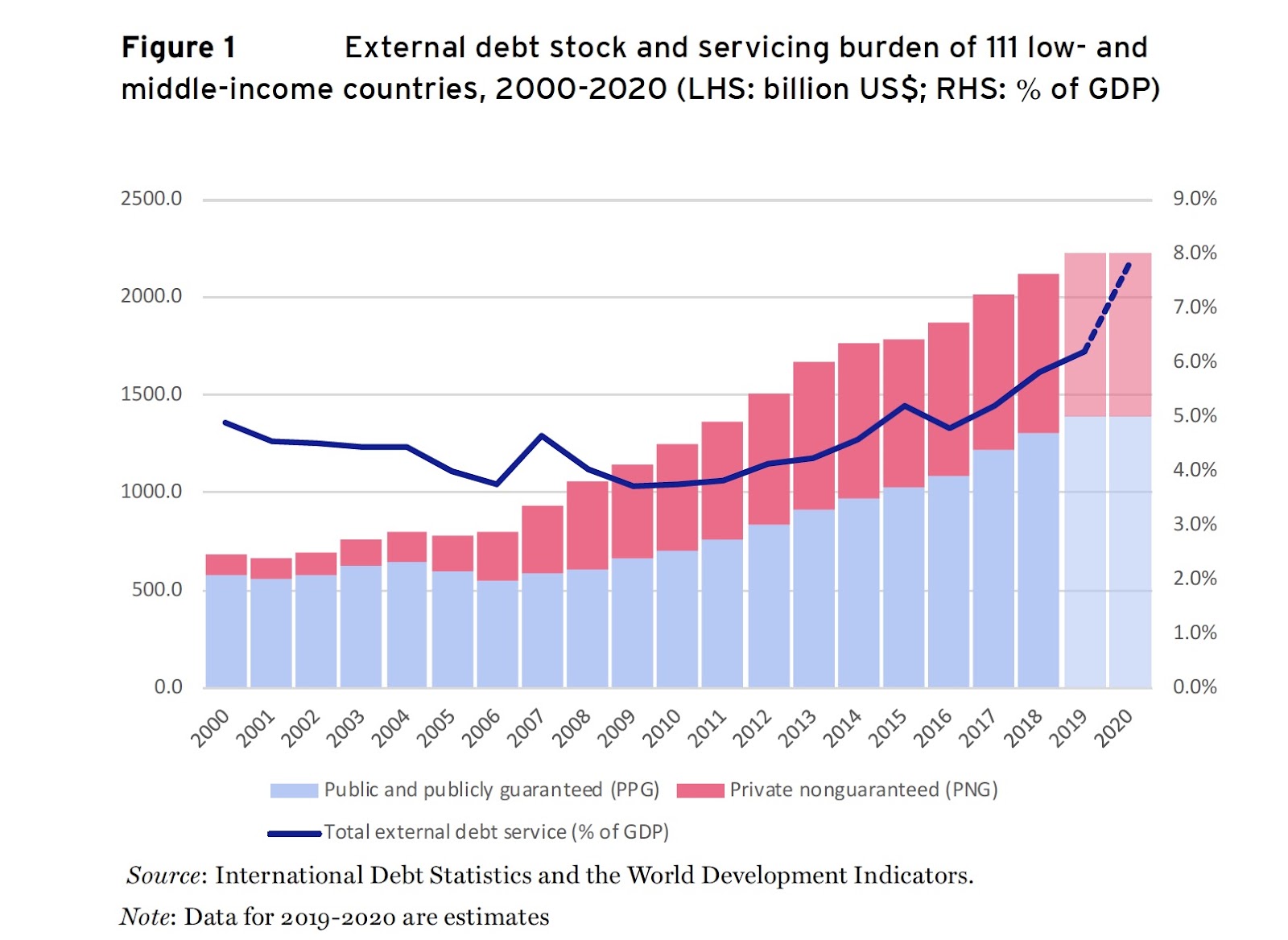

However, the debt problem comes as no surprise to many. The 2008 financial crisis marked the beginning of a massive increase in sovereign bond issuance amongst low and middle-income states struggling to control their debt in an international economy refusing to provide assistance. Since then, debt levels in developing countries have tripled, in large part because new lending options for debt-ridden countries were higher and came with more restrictions than previous concessional market rates. As a result, total debt in emerging economies at the end of 2019 stood at $55 trillion according to the World Bank. Responding to a 2019 report entitled “Global Wave of Debt,” World Bank President David Malpass said, “The size, speed, and breadth of the latest debt wave should concern us all.”

Worse still, many developing countries facing the coming debt crisis are heavily reliant on export markets that have been severely affected by the pandemic. The World Trade Organization anticipates a reduction in trade by the end of the year of about 9.2 percent globally in combination with a 4.8 percent reduction in overall GDP. Unfortunately, export financing is a major way by which developing countries are able to finance their debt, a reality that threatens to exacerbate an increasingly limited pool of potential creditors in 2020.

In response to the crisis, the G20 has requested a halt in interest payment collections from low and middle-income countries during the fiscal year, and the World Bank has asked its major donors to cease requesting interest payments from countries benefiting under IDA lending programs. According to the OECD, the G20’s debt collection halt could have a value of $25.3 billion if properly implemented, though this represents only a very small fraction of the total public debt interest developing countries will be required to pay to bilateral and multilateral lenders. In response, the World Bank and IMF have asked the G20 to “prepare a proposal for comprehensive action by official bilateral creditors to address both the financing and debt relief needs of IDA countries.”

To assist the G20 in pursuing their relief goals, the World Bank committed $8.1 billion to the Debt Service Suspension initiative, the majority of which is to be financed with grants. They also promised to increase their grant lending to IDA countries to help relieve social and financial pressures caused by the COVID-19 pandemic. President Malpass said of the program in a September speech, “As of mid-September, 43 countries were benefiting from an estimated $5 billion in debt-service suspension from official bilateral creditors, complementing the scaled-up emergency financing provided by the World Bank and IMF.”

Similarly, the IMF has extended the amount of pandemic relief funding by doubling the size of its Rapid Financing Instrument Fund and the establishment of a Short-Term Liquidity Line, which is designed to increase the financial lending quota by 145 percent for countries with short-term capital needs. Much of the IMF’s debt relief has come in the form of the Catastrophe Containment and Relief Trust (CCRT), which is financed jointly by the bank and donors. The CCRT received a mandate in March—and a recent extension in September—to assist 28 of the world’s most financially vulnerable countries by providing debt service in the form of grants and extreme concessional loans.

As of mid-September, 14 developed countries had dedicated just over $1.4 billion to help finance the CCRT, with a second round of financing coming later this year. While this represents a strong initial showing from multilateral financial institutions, the amount of relief offered at both the bilateral and multilateral levels must significantly increase in the coming months to avoid a potentially decades long slippage into a global debt burden.

Paying a Way Out

With limited recourse and pressure to avoid default, what can countries facing crippling debt turn to in the current crisis? A variety of solutions exist, some simply involve increasing the size and scale of current lending programs and debt relief policies. Others recommend a total rethinking of the way international lenders view debt rehabilitation.

Increasing the scale of current debt relief programs has been largely discounted by the United Nations, World Bank, and IMF as a long-term debt reduction strategy because current policies have aimed at halting debt repayments rather than actually paying down the debt. While halting repayments was a productive short-term solution for avoiding default early in the pandemic, the scale of the coronavirus has made it clear that full-scale debt restructuring and increased capital injection will likely be required to keep developing nations from collapsing under their debt burdens.

To that end, multiple organizations have moved to expand their lending capacities to support social programs and financial restructuring in response to coronavirus related disruptions. The IMF pledged to make “make available” a $1 trillion lending capacity to help member countries cope with pandemic fallout. So far, just over $100 billion has been extended to 89 member countries in the form of financial relief programs. In March, the G20 also agreed to inject $5 trillion globally “as part of targeted fiscal policy, economic measures and guarantee schemes.”

The United Nations Conference on Trade and Development (UNCTAD) lauded these efforts, but recommended international organizations consider internal restructuring to streamline their ability to raise and extend capital. These recommendations included reallocating the IMF’s Special Drawing Rights—a unit of account used to favor wealthier nations—so that more developing countries could benefit from IMF financing over the course of the next several years. The same report also stressed the importance of meeting Official Development Assistance (ODA) flows, which are guarantees of financing by wealthy nations to developing countries. “An additional $2 trillion would have reached developing countries had the 0.7 per cent (of global national income)” benchmark been met by ODA lenders between 2010 and 2020, UNCTAD concludes.

However, throwing money at the problem is not necessarily the most effective way to solve a debt crisis. Steps taken to halt debt interest repayments earlier this year will not be enough to keep low and middle-income countries from beginning to default. The $4.482 trillion in repayments owed by developing countries that were postponed by the World Bank and IMF will still be due between 2022 and 2024. According to the Centre for Economic Policy Research, “A standstill … is just short-term palliative; these measures are, at most, band-aids for a much larger systemic problem.”

Long-term solutions to debt crises at the national level focus on reducing the financial stress of debt caused by sovereign bonds. Much of this would include the regulation of sovereign bond cash-ins and buybacks to avoid bank runs and government defaults. Rewriting financial laws to include force majeure clauses, which exclude natural disasters as grounds for receiving overly high interest rates on debt bonds, and to prohibit buying massively discounted bonds would also minimize the volatility of sovereign debt bonds.

At the international level, a full reimaging of debt-restructuring financing may be in order. As Nana Addo Dankwa Akufo‑Addo, President of Ghana, said to the United Nations, “It is vital to restructure the global financing architecture to enable fresh financing to developing countries as an immediate necessity.” A report by the United Nations recommended that multinational financial institutions like the World Bank consider extending concessional lending terms to non-IDA countries (middle-income countries) for the purpose of making debt relief packages more appealing to governments while also reducing already concessional lending terms among IDA countries. Another inventive idea is to incentivize COVID-19 response through debt-to-COVID swaps, which would forgive government debt in return for investments in healthcare and pandemic prevention infrastructure.

A number of calls have also been made for private lenders to stall their debt payment requests and consider contract renegotiations in light of the pandemic. Private creditors make up a significant portion of debt externalities in low and middle-income countries, but they are often the least flexible lenders when it comes to repayment conditions. World Bank President David Malpass affirmed, “Private creditors and non-participating bilateral creditors should not be allowed to free-ride on the debt relief of others, and at the expense of the world’s poor.” Outside of requesting creditors abide by the Debt Service Suspension Initiative (DSSI), however, little legal action has been taken by international groups to force private creditors to comply with global norms. While much lip service has been given to the idea of rethinking multilateral debt relief, little action has been taken.

Take Home Points

The international community likely has only several months remaining to effectively coordinate a comprehensive debt-relief strategy for developing countries. A complete response to the crisis should include the following.

1. A reimagining of lending at the sovereign and international level, including expanding funding for developing countries at increasingly concessional rates.

2. The improvement of current debt relief structures to allow borrowing countries faster access to relief funding and increase the lending potential of every dollar.

3. A reimagining of what debt refinancing looks like, including the use of even lower concessional rates and potentially leveraging partnerships with private lenders and novel financial lending instruments.

Admittedly, having a discussion about the details of international loans and national debt is neither glamorous nor apparently relevant. And with everything else going on in the world in 2020, it’s easy to ignore skyrocketing debt in developing countries as just another crisis in a crazy year. But, the reality is, unless international organizations and wealthy nations around the world work together to minimize the impacts of financial freefall in low and middle-income countries, the resulting scale of human suffering over the next decade is likely to be incomprehensible.

Without support, developing nations will not be able to pay the bills. When governments can’t pay, it is their people who bear the burden. It is up to international organizations and wealthy nations to mitigate this possible human catastrophe. As the Managing Director of the IMF Kristalina Georgieva remarked, “It is up to us to build forward better.”