Author: Valentina Alvarez Demalde

The BRB Bottom Line: Argentina, a country often plagued by economic turmoil and political instability, is no stranger to the challenges of managing its domestic currency. The nation’s history is marked by cycles of hyperinflation, currency devaluation, and economic crises. In this context, the concept of dollarization, which involves adopting the US dollar as a substitute or parallel currency to the domestic peso, emerges as a compelling proposition.

Introduction

What is Dollarization?

To evaluate this shift, we must first understand why dollarizing an economy arises as a solution. This method represents the adoption of the US dollar as the primary medium of exchange or official currency in a country. It can be implemented as an official government policy or embraced de facto by the people. While this shift is often considered in situations where a nation’s domestic currency faces severe depreciation or becomes unreliable due to hyperinflation and instability, it’s important to note that dollarization is just one of several potential responses to such economic challenges. It may also be the case that domestic authorities have proven themselves incompetent to manage their own monetary policy, which Milei argues is the case for Argentina’s political landscape.

Argentina’s Political Landscape

In recent times, this political stage has witnessed a shift. The traditional divide between the center-left Peronist coalition and the center-right opposition has been disrupted by the emergence of a new political force led by Javier Milei, a self-proclaimed liberal economist and author. Milei, representing the independent political party “La Libertad Avanza” (Liberty Advances), managed to secure over 30% of the votes in both the primary and general elections, ending up first and second place and heading for a “ballotage” with the center-left. The far-right has won this ballotage against the center-left, clearing 56% and 44% respectively, meaning Javier Milei will be the president of Argentina starting December 10th. This surprising political shift can be attributed to a growing discontent with past governments, seen as ineffective and corrupt (as Vice-President Cristina Kirschner faces charges of “fraudulent administration”). This context has created an opening for Milei, presented as a political outsider and symbol of opposition to corruption, to pose a vision for the country’s future, one that includes the potential adoption of the US dollar as the national currency.

Discussion & Findings

Argentina’s Economic History

Argentina’s economic history, marked by cycles of instability, is key to understanding the significance of dollarization and Milei’s vision. The country’s early prosperity, based on agricultural exports, gave way to economic shifts through the 20th century. The Great Depression impacted commodity prices, leading to Perón’s protectionist policies. Later, political turmoil and policy fluctuations characterized the mid-century. The 1980s and 1990s saw hyperinflation and currency crises, culminating in the Convertibility Plan’s failure and a severe debt crisis. Recent presidencies, from Mauricio Macri’s market liberalization to Alberto Fernández’s interventionist policies, have continually grappled with inflation and fiscal challenges. This backdrop underscores the potential of unconventional strategies like dollarization to address persistent economic issues and government mistrust. The paper employs a thorough methodology, including data analysis, literature review, and expert insights, to assess dollarization’s viability for Argentina.

Javier Milei’s Plan

Javier Milei’s vision for Argentina is centered on abolishing Argentina’s Central Bank, which stems from his belief that this entity has a history of “robbing the people” by ineffectively managing monetary policy and printing more money, devaluing the peso. He emphasizes a gradual approach to dollarization, driven by individual and business choices, with an automatic shift once two-thirds of the monetary base adopts the U.S. dollar. This flexible approach allows the transition to align with the preferences of the Argentine population. Milei suggests funding this transition using the government’s financial reserves and the sale of Central Bank bonds. In terms of political processes, Milei’s plan is unique in that he proposes allowing the people to decide through a plebiscite if Congress previously rejects the plan. He also emphasizes a focus on free trade, peace, freedom, and aligning with Western countries, particularly the US and Israel, while showing reluctance toward relations with communist nations like China and Venezuela.

Dollarization Pros & Cons

Dollarization as a potential economic strategy for Argentina presents several compelling advantages. Foremost, it promises currency stability and inflation control, a precious commodity in a nation with a history of hyperinflation and devaluation. This stability can instill trust among investors and the public, offering a predictable economic environment. With a stable U.S. dollar, Argentina may enjoy lower interest rates, a boon for businesses and individuals alike, making borrowing more affordable. Furthermore, adopting the U.S. dollar can attract foreign investment, with investors favoring countries with stable and widely accepted currencies. This influx of foreign capital can stimulate economic growth. Additionally, businesses engaged in international trade would benefit from reduced transaction costs, as they would no longer need to navigate currency exchange. Finally, dollarization can promote financial integration with the global economy, potentially increasing trade and investment in Argentina.

Dollarization in Argentina presents several potential drawbacks. Most notably, it entails relinquishing control over domestic monetary policy, a vital tool for governments to manage economic challenges— Milei sees this as an advantage due to a lack of trust in the government’s management. The prospect of dependence on the U.S. economy is concerning, as it would make Argentina vulnerable to U.S. economic fluctuations and shocks. However, Milei’s plan to increase trade with the U.S. aims to address this issue. Dollarization also carries a risk of exacerbating short-term social inequality, as those with access to U.S. dollars may initially benefit, although proponents like Milei argue that the long-term effects of a stable economy will ultimately improve the overall situation of society. The loss of seigniorage, while viewed as a pro by some, poses a significant drawback as it could limit the government’s capacity to fund public spending. Finally, the transition to a dollarized economy could trigger political unrest and opposition from stakeholders invested in maintaining the status quo.

Case studies: Ecuador & El Salvador

Two LATAM countries serve as valuable case studies for insights into the potential outcomes and challenges associated with the adoption of dollarization as an economic strategy.

Ecuador’s implementation of dollarization in 2000 followed a “Big Bang” approach. This involved replacing the former currency, the sucre, with the U.S. dollar at a fixed exchange rate of 25,000 sucres to 1 dollar. The transition was completed in a swift nine months. Ecuador’s experience demonstrates the feasibility of a rapid and decisive shift to the U.S. dollar as the official currency. On the other hand, El Salvador’s dollarization in 2001 pursued a more gradual approach, enacting the Monetary Integration Law. This law fixed the exchange rate at 8.75 colones to 1 U.S. dollar. This transition spanned approximately 24 months. While the former alternative could be executed faster, the latter resembles Milei’s more flexible, gradual, and less drastic plan for dollarization.

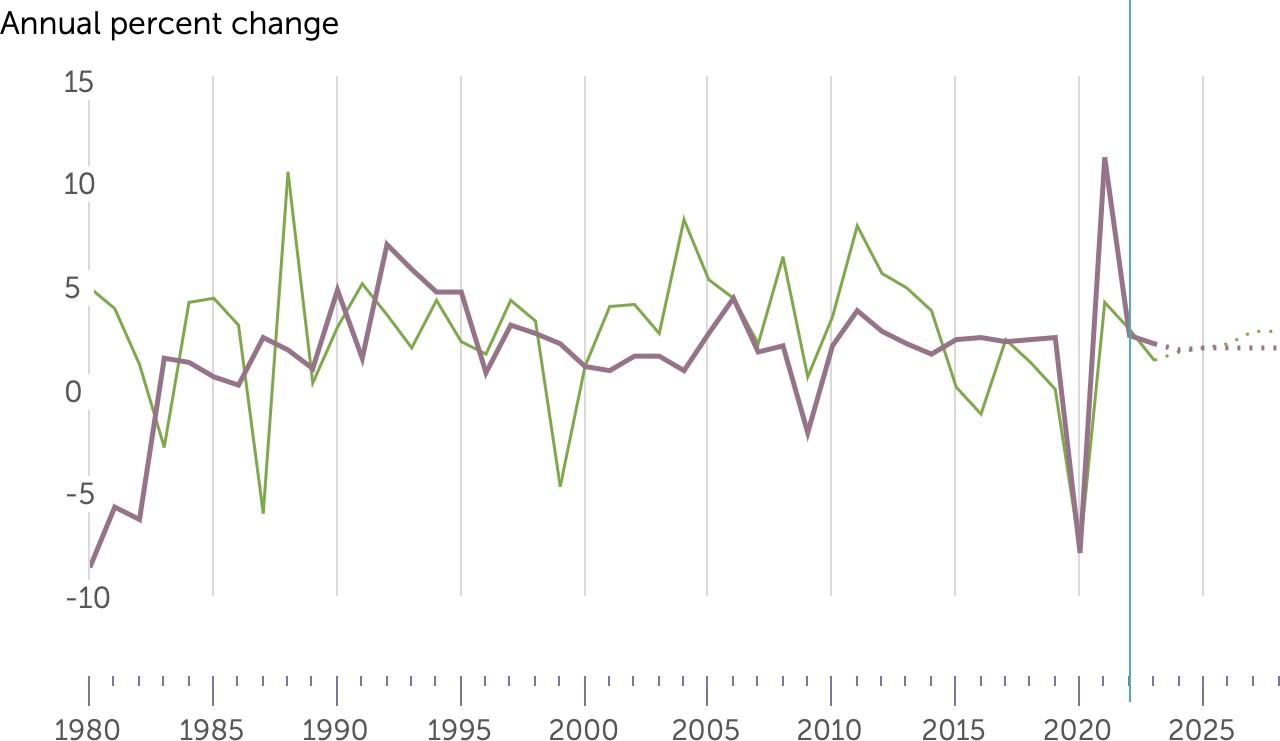

Figure 1. Real GDP Growth (IMF) for Ecuador (green) and El Salvador (Purple)

The graph depicting the Real GDP growth of both countries over time is a helpful visual representation to analyze the impact of dollarization on these economies. For Ecuador, dollarization was implemented in the year 2000. Looking at the green line, we see a clear upward trend in growth rates which suggests a positive impact from dollarization. Similarly, El Salvador dollarized its economy in 2001. We can see reduced volatility and increased stabilization in the growth rate with a slow upward trend at first, indicating an improved economic condition. While dollarization can influence economic stability and growth, many other factors also play critical roles, including global economic conditions, domestic policies, and structural changes in the economy. For example, in both cases, the Global Financial Crisis of 2008 and the Global Pandemic of 2020 caused negative fluctuations in GDP Growth.

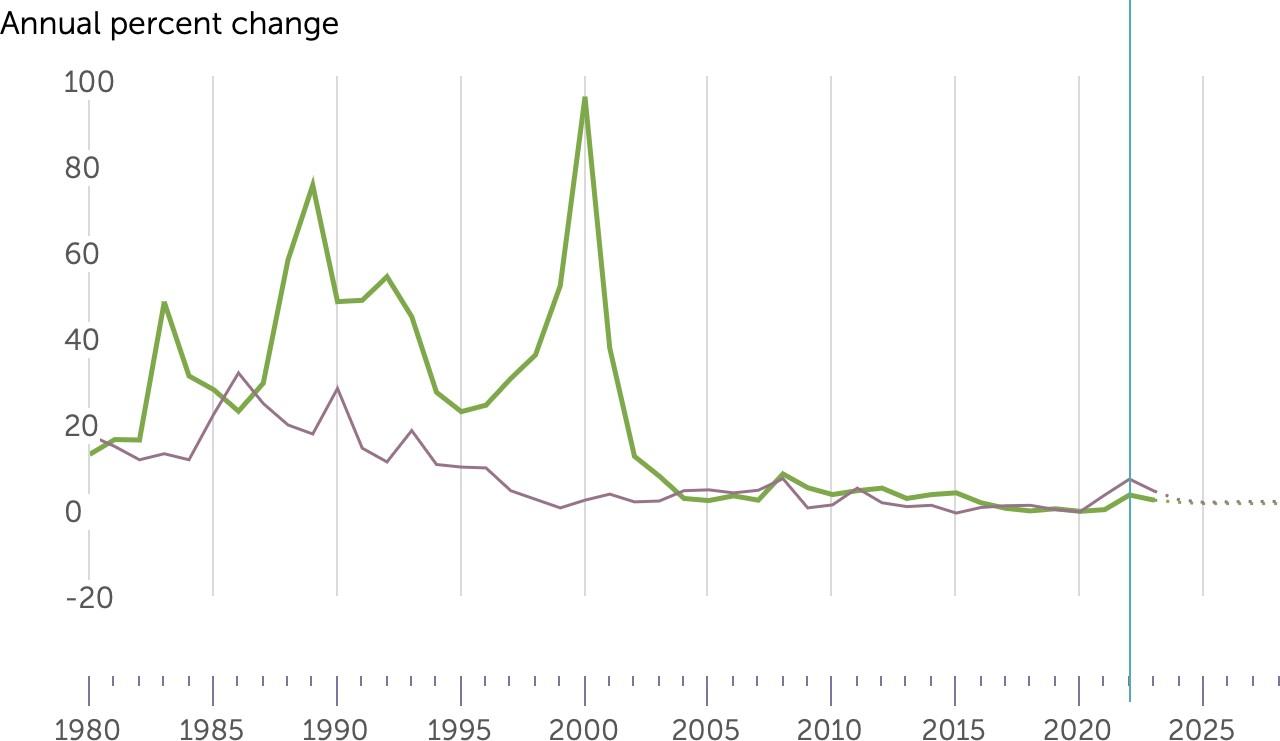

Figure 2. Inflation Rate, Average Consumer Prices (IMF) for Ecuador and El Salvador

Upon examining the provided graph for the inflation rates in Ecuador and El Salvador, we observe the impact of dollarization on their economies through changes in the annual percent change of inflation. For Ecuador, which adopted the dollar in 2000, the graph’s green line demonstrates an indisputable downward trend and stabilization in inflation rates post-dollarization. This clear drop in inflation immediately following dollarization, transitioning into a stable, low rate in the subsequent years depicts the implementation’s success. The consistency of this trend reinforces the argument that dollarization contributed to inflation control in Ecuador. Turning to El Salvador, with the purple line representing its post-2001 dollarization inflation rates, we do not see an evident decrease in the rate of inflation but a slightly more stable trend.

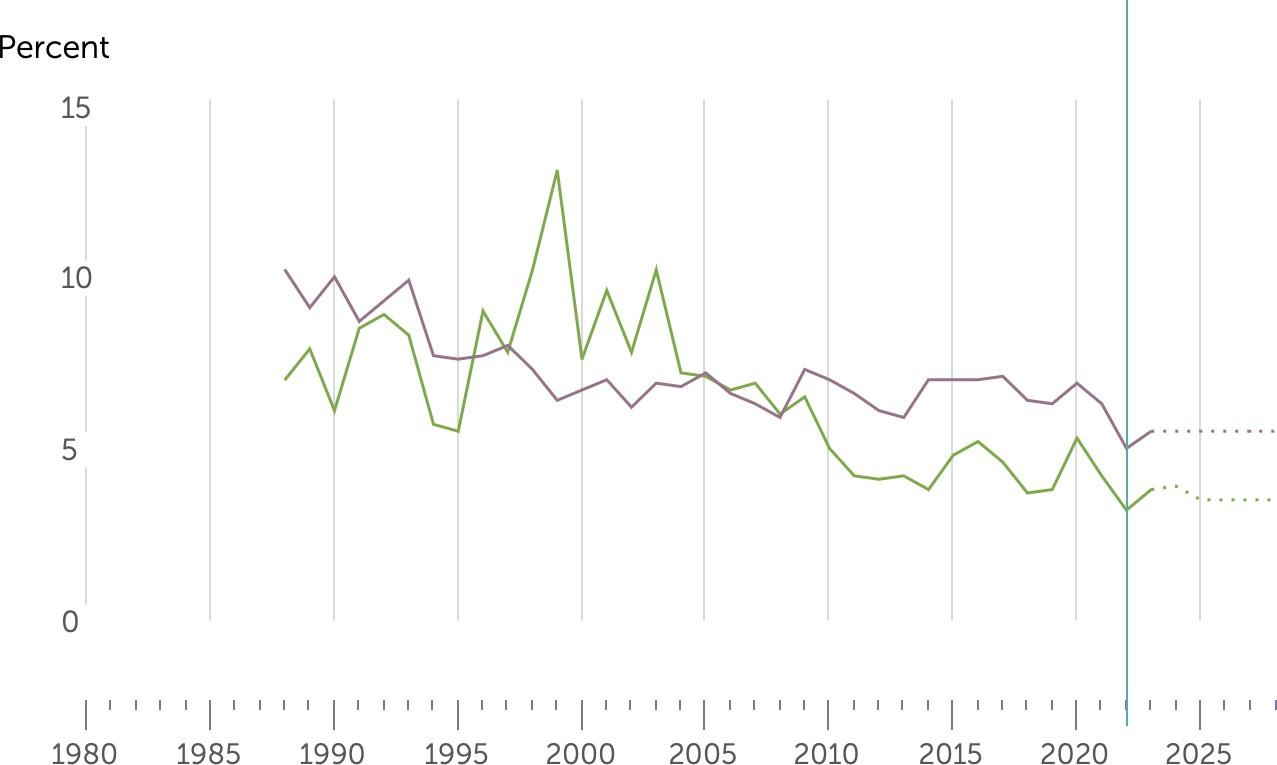

Figure 3. Unemployment Rate (IMF) for Ecuador and El Salvador

In terms of the unemployment rate, Ecuador reflects how dollarization helped stabilize the economy and lead to job creation, indicated by a declining trend in the unemployment rate after 2000. The period immediately following dollarization may show some volatility as the market adjusts, but the long-term decrease or stabilization at a lower unemployment rate suggests the positive impact of dollarization on the job market. Once again, in the case of El Salvador, after adopting the dollar in 2001, the purple line shows no evidence of clear decreased unemployment. This might suggest that dollarization alone was not sufficient to improve job creation, or that other significant economic or structural challenges offset the potential benefits of dollarization.

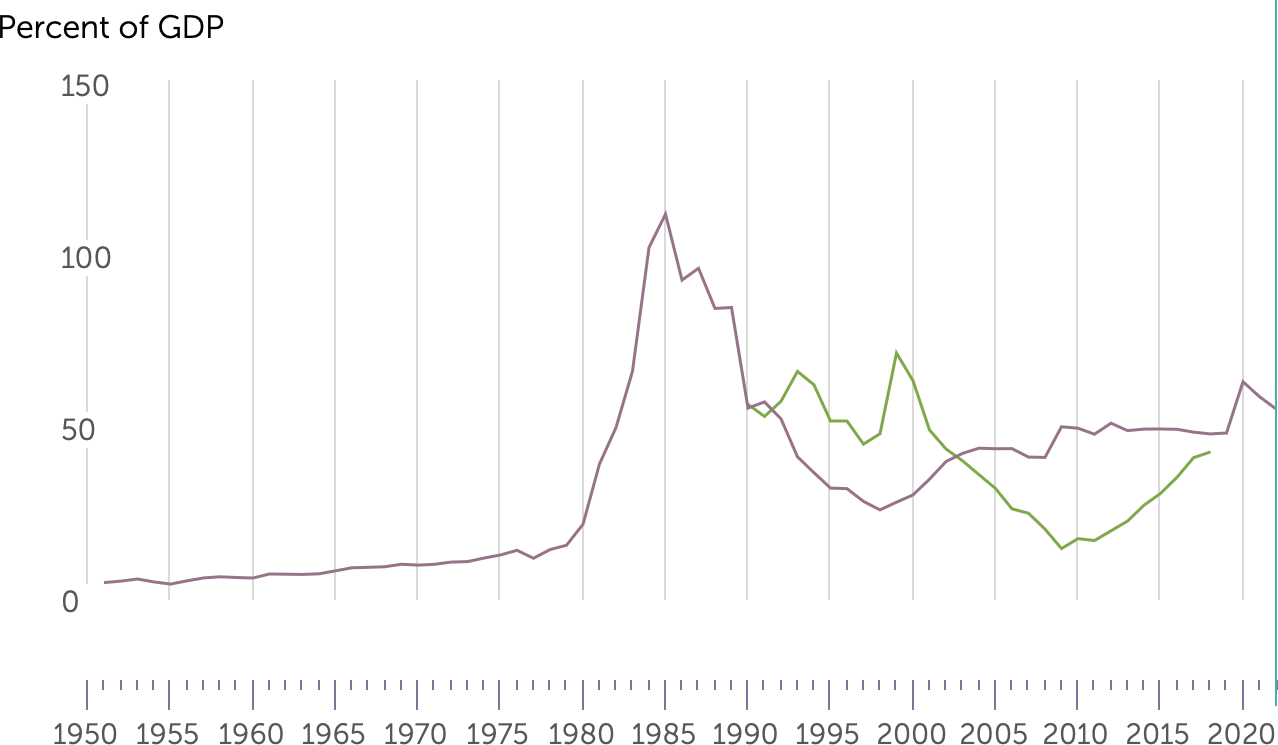

Figure 4. Central Governmental Debt (IMF) for Ecuador and El Salvador

The central government debt as a percent of GDP for Ecuador (green) and El Salvador (purple) provides valuable insights into the fiscal impact of dollarization on these economies. For Ecuador, dollarization in 2000 was followed by a reduction in the debt-to-GDP ratio as seen on the green line on the graph. This decreasing trend suggests that the government’s fiscal health improved post-dollarization, possibly due to reduced borrowing costs or better access to international financial markets. In contrast, El Salvador’s purple line does not show a similar trend of stabilization indicating that other factors were at play that influenced the country’s debt levels. A reason might be that for El Salvador, if the debt was previously denominated in a local currency that depreciated, dollarization might instantly increase the local currency value of foreign debt.

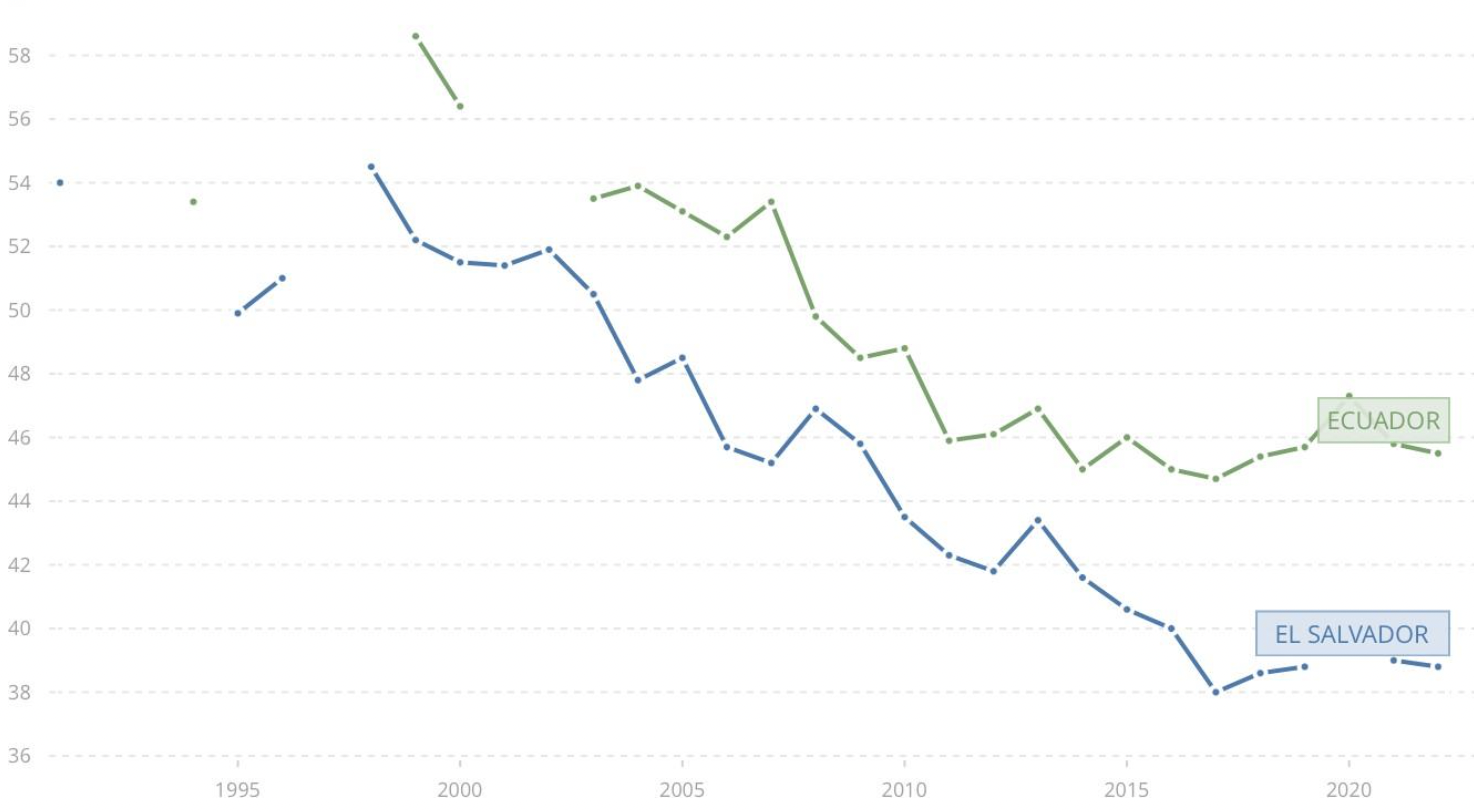

Figure 5. Gini index – El Salvador, Ecuador (The World Bank)

Lastly, the Gini coefficient is a measure of income or wealth distribution within a nation, where a lower Gini coefficient indicates a more equal distribution and a higher coefficient points to greater inequality. Based on the graph provided, it seems that Ecuador and El Salvador both show a downward trend over the years, suggesting a reduction in income inequality. However, attributing this solely to dollarization would require ruling out other influences like economic policy shifts, globalization, technological changes, demographic shifts, and educational access improvements. So without comprehensive analysis, it’s challenging to link these changes directly to dollarization.

In essence, dollarization has delivered mixed results in Latin America. As seen in the graphs, Ecuador found some stability through it, but El Salvador’s journey since 2001 suggests that dollarization alone doesn’t guarantee economic growth (as it was not struggling with hyperinflation in the first place). For Argentina, considering its hyperinflation dilemma, Ecuador’s experience becomes more relatable. Yet, El Salvador’s story is an example underscoring that without addressing underlying issues like social unrest, dollarization may not attract the investment or deliver the economic growth hoped for.

Conclusion & Alternative Policies

In conclusion, Argentina finds itself at a pivotal crossroads, grappling with persistent economic challenges and recurrent crises. The proposal of dollarization by Javier Milei represents a bold avenue for the nation. It offers the prospect of currency stability, which is vital given Argentina’s history of hyperinflation and devaluation. While relinquishing control over domestic monetary policy and economic dependence on the U.S. are key concerns, the case studies of Ecuador and El Salvador shed light on potential strategies for successful implementation. If Argentina were to dollarize, the government should make well-informed decisions, actively engage with the public, and ensure economic stability, social equity, and international competitiveness. Argentina has experimented with several alternative economic policies in its quest for stability, including pegging the currency to another stable currency, managing float exchange rates, capital controls, and promoting the use of the local currency. Having utilized these approaches to varying degrees, the consideration of dollarization in the country’s economic strategy shows a need for a fresh perspective in light of Argentina’s recurring economic challenges and the potential benefits that a stable, widely accepted currency can offer. In this vital chapter of Argentina’s economic history, Javier Milei’s upcoming presidential cycle holds the key to the nation’s future, demanding effective decision-making and governance for a stable economy and a better future for Argentinians.

Take-Home Points:

- Dollarization in Argentina: the adoption of the US dollar in place of a national currency is considered in Argentina as a response to economic instability and hyperinflation.

- Javier Milei’s Influence: his election as president, representing the far-right “La Libertad Avanza” party, indicates a significant political shift in Argentina, with a focus on radical economic reforms.

- Economic Context and Milei’s Plan: Argentina’s history of economic crises provides a backdrop for Milei’s proposal of gradual dollarization, emphasizing free trade and alignment with Western values.

- Pros and Cons of Dollarization: Dollarization can offer stability and lower inflation, but also poses risks like loss of monetary policy control and dependence on the US economy.

- Lessons from Ecuador and El Salvador: Case studies of Ecuador and El Salvador show varying outcomes of dollarization, suggesting its effectiveness depends on specific economic conditions and policies.

- Future Economic Strategies: Argentina’s exploration of dollarization reflects a promising search for solving ongoing economic challenges, with a need for a new perspective.