Rate Cuts and Rate Cuts and Rate Cuts and Tate McRaete

Authors: Andres Larios, Jay Sahaym

Story of the Week: Praniti Gulyani

Intro:

Welcome to the Weekly BluRB, a newsletter catered to students and professionals to get the latest news and insights on global markets. Get prepared for the week by reading four weekly stories circulating around equity markets, macro trends, geopolitics, and new business developments. And the best part: we’ll give you an informed view about where we think prices, policy, and trends are going in the near future. The content in these writings is for informational purposes only and does not constitute financial or investing advice.

Last Week’s Calls:

Dell Stock on the Rise – Up 6.37% in Last 5 Days

Palantir Stock on the Rise – Up 8.77% in Last 5 Days

25 bp Fed rate cut – 50% Probability, 87% Probability Peak on Wednesday/Thursday

Oil Prices on the Rise (eventually) – Crude Oil Futures up 0.69% in Last 5 Days (Thesis played out early due to Hurricane Francine). Expect downward price adjustment next week.

Equity Markets: SMid-Caps Rule and Oracle Guidance Drive Strong Weekly Performance

The stock market was strong this past week due to rate cut anticipation. What do rate cuts mean for stocks and why has this caused equity markets to rally? Interest rates determine short term borrowing costs and at the current target rate of 5.33% puts an added strain on equity present value, as well as on many companies who fund their operations with large portions of debt. This quarter, we have seen SMid-cap stocks outperform the S&P 500, showing that investors are bullish on the stocks that are most affected by high interest rates.

With a rate cutting cycle set to begin this week, we’ve seen a historic week for the S&P 500 and the Russell 2000 index respectively. Two weeks ago, the S&P 500 experienced its worst week of the year, but markets seem extremely optimistic about what cutting rates is going to mean for large cap businesses as the index rose 3.38% for its best week of the year. This is important because on the large-cap side, investors are diversifying away from the Mag-7 stocks that rallied the stock market in 2024 (and who have now slumped in the past two months).

The effect is greater for the Russell 2000, an index that tracks small-cap stocks, seeing as the index rose 4.27% this past week. The signal we are seeing is that investors are now positioning themselves for companies that may have been overlooked due to mounting debt pressures, but who have high growth outlooks.

The stock we are looking at this week is Oracle. With a market cap of $450 billion, we see the potential for the company to push past a valuation of $1 trillion in the coming years due to their cloud sales popping off and its growth into data center infrastructure (Stock rose 13% this week). Since Oracle’s founding, it has been an industry leader in database software and a trailblazer in cloud computing. This week, founder and CTO (and former Berkeley resident), Larry Ellison announced that Oracle is building nuclear reactors to power its automated GPU clusters adding to long term hype behind the stock and its role in the AI revolution.

US Macro: Is This the Soft Landing We Were Hoping For? Lessons from the Housing Market

This is the week for rate cuts! The target Federal Funds Rate has been 5.25-5.50% for over a year now in an effort to contain post-pandemic inflation. On September 18th, Chair Powell will almost surely announce a rate cut. The question of how aggressively is still up in the air as market-makers are still pricing in a 50% chance of a 50 bp cut (we think this is a pump and dump scheme). Last week, we predicted a 25 bp cut, and we maintain that view, especially as we dig through recent inflation data.

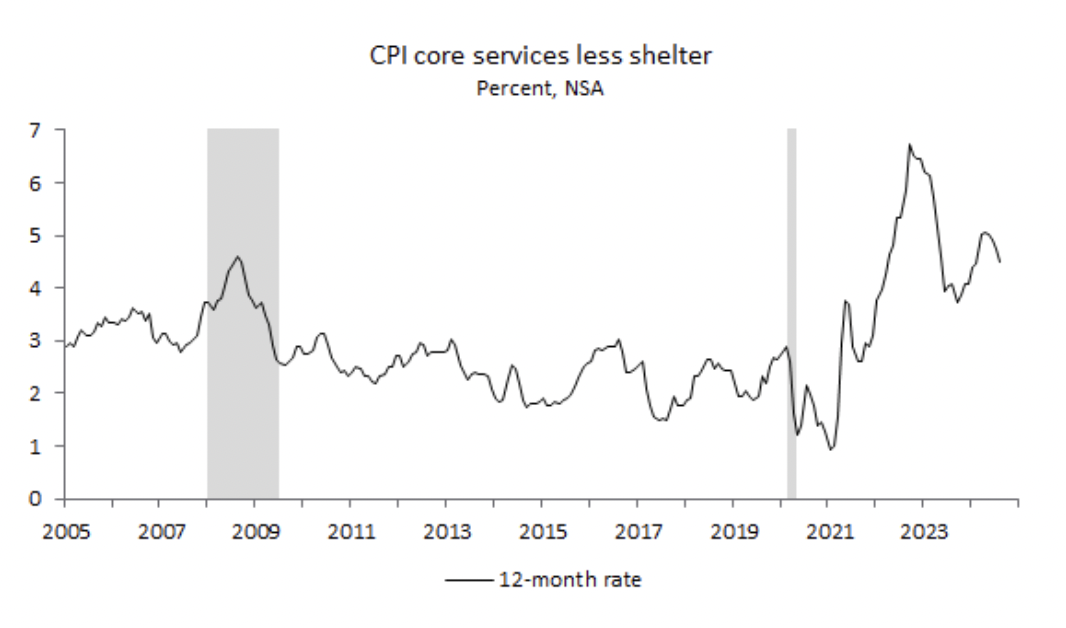

This Chart Shows that Core Inflation is Nowhere Near the Fed’s 2% Target

CPI, which measures the changes in prices paid by US consumers, is one of the more favored inflation data points by the Federal Reserve. And this chart, that measures core services excluding housing while accounting for 28% of the consumption basket measured, is concerning for two reasons. Core services exclude food and energy because their prices are seen to be more volatile. Thus, underlying core services are seen to be a more accurate representation of the true demands of the American consumer. Seeing how core services (less shelter) unexpectedly picked up in the latest CPI Report, we think this is conclusive evidence to rule out a 50 bp rate cut.

When considering housing, shelter prices increased 0.5% in the past month. This sticky inflation is particularly concerning when thinking about the American consumer and the accompanying job’s data mentioned in last week’s BluRB (notably downward revisions). MBS yields have fallen to one-year lows, but construction costs remain high and housing prices remain excruciatingly high. Thus, mortgage applications are still at 5-year lows despite incoming rate cuts and lowering mortgage rates. As credit becomes more accessible to the average American, housing supply is not at the point to grow symmetrically with demand, meaning there is no downward pressure in the housing market, despite the expected change in policy.

Accordingly, we still believe it is the time to cut rates and 25 bp is an adequate amount, however, we do not think the Fed, nor the state of the US economy is in a good position at all. Is this a soft landing? Hopefully, but it will be a rocky one.

Global Macro: Groundbreaking Plans from Europe’s Godfather and Godmother

The European Central Bank (ECB) cut interest rates by 25 bp for Eurozone countries this past Thursday, making their target rate 3.5%. ECB President, Christine Lagarde, cites the successful curbing of decade-high European inflation, and ~slight fears of slowing consumer demand. Experts believe that high European wage growth won’t affect inflation and instead companies will accept lower marginal profits.

However, the Eurozone is focusing on the Draghi Report. Mario Draghi, former President of the ECB outlined an $800 billion investment plan to reinvigorate Europe as an economic hub. This amount is more than double the amount invested in The Marshall Plan in the wake of the destruction of World War II. Draghi praises the economic structure of the United States and encourages Europe to emulate many policies such as the Inflation Reduction Act. Draghi’s goal with this plan is to stimulate research and technology efforts in Europe so that businesses can start, grow, and stay in Europe throughout changing geopolitical and trade dynamics. Draghi states Europe will face a “slow and agonizing decline” if these measures are not implemented.

European Investment Sentiment Index

Implementation, however, will be difficult as Germany, unofficial leader (and lender) of the EU has raised doubts on the report’s method of funding. Draghi proposes collective EU borrowing to fund this massive investment project. Although important figures like ECB President Lagarde and Thomas Piketty have endorsed the report, fiscally healthy countries like Germany and the Netherlands fear this collective borrowing will ultimately weigh on them more than other members of the EU. Further inflation concerns from such large investment operations have also been highlighted.

Moving across the English Channel, we expect the Bank of England to hold rates steady at 5% on Thursday.

Story of the Week: Kidnapping Scares You? The World’s Greatest CEOs Are Scared, Too.

While life as a Tech CEO might appear ideal, it comes with a considerable amount of challenges. Personal security has become a significant— and immensely expensive— part of daily life. As per an article by Yahoo News, Bill Herzog, the CEO of Arizona-based LionHeart Security Services emphasized the importance of “protecting someone who is worth millions or billions of dollars and is in charge of an entire company.” Herzog goes on to state how his company would charge $60 an hour or more— making the total expenditure $1 million per year for just two guards.

As per previous statistics, Meta spent over $23.4 million to ensure Mark Zuckerbeg’s personal security. For protecting the cost of their CEOs, Apple reports a cost of $0.8 million, Tesla reports $2.4 million, Nvidia reports $2.2 million and Alphabet reports a whopping $6.8 million. These exorbitant costs are not without reason. In the last eight months, Elon Musk reported two assassination attempts describing how the potential assassinators were arrested with guns just 20 minutes away from Tesla’s Gigafactory in Austin, Texas—leading him to consider building a flying metal suit of armor.

The increased demand for outsourced security services has also led to a widespread increase in the valuation of the private security market from $224.49 billion in 2022 to $235.37 billion in 2023. Furthermore, the market is predicted to be worth $338.23 billion in 2030, meaning the expected CAGR during the forecast period is between 5.3-7.8%. This figure lingers close to the global cybersecurity CAGR of 9.8%, depicting a high growth rate, as well as how security— in the general sense of the term— is a broadly growing market.

Make sure to tune in next week for more market updates and global insights!