Are the Hawks Too Hawkish? – Lessons from China and the Stock Market

Authors: Andres Larios, Jay Sahaym

Story of the Week: Mauricio Chandler

Intro:

Welcome to the Weekly BluRB, a newsletter catered to students and professionals to get the latest news and insights on global markets. Get prepared for the week by reading four weekly stories circulating equity markets, macro trends, geopolitics, and new business developments. And the best part: we’ll give you an informed view about where we think prices, policy, and trends are moving in the near future. The content in these writings is for informational purposes only and does not constitute financial or investing advice.

Last Week’s Calls:

Talen Energy Overweight – -2.48% (watch it grow)

Fed 25 bp cut – 38 days to go

China to cut rates – Cut three major rates after our BluRB

Equity Markets: Macro Data Drives the Bull Market and MS Call Obliterates US Autos

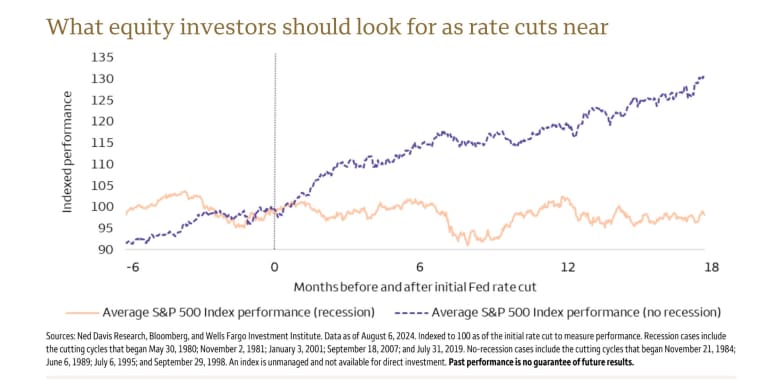

The stock market was strong this past week, but mostly because there wasn’t too much movement. The S&P 500 and Dow Jones Industrial Average held record highs this week, but the Russell 2000, an index for small and mid-cap names, fell by roughly 0.28%. The Fed’s decision a week and a half ago definitely contributed to these higher equity valuations, but are these prices going to plateau?

Friday morning, September PCE data was released, showing that inflation rates are falling. PCE increased 2.2% in the past year, which was below the Wall Street consensus, supporting further rate cuts down the line. It’s pretty clear to see that this bull market is being driven by macro news. While US equity prices might not continue to rise as aggressively as in the past few months, loose monetary policy should allow projections for stock prices to increase throughout the rate-cutting cycle.

Chart 1: S&P 500 Performance After Initial Rate Cut

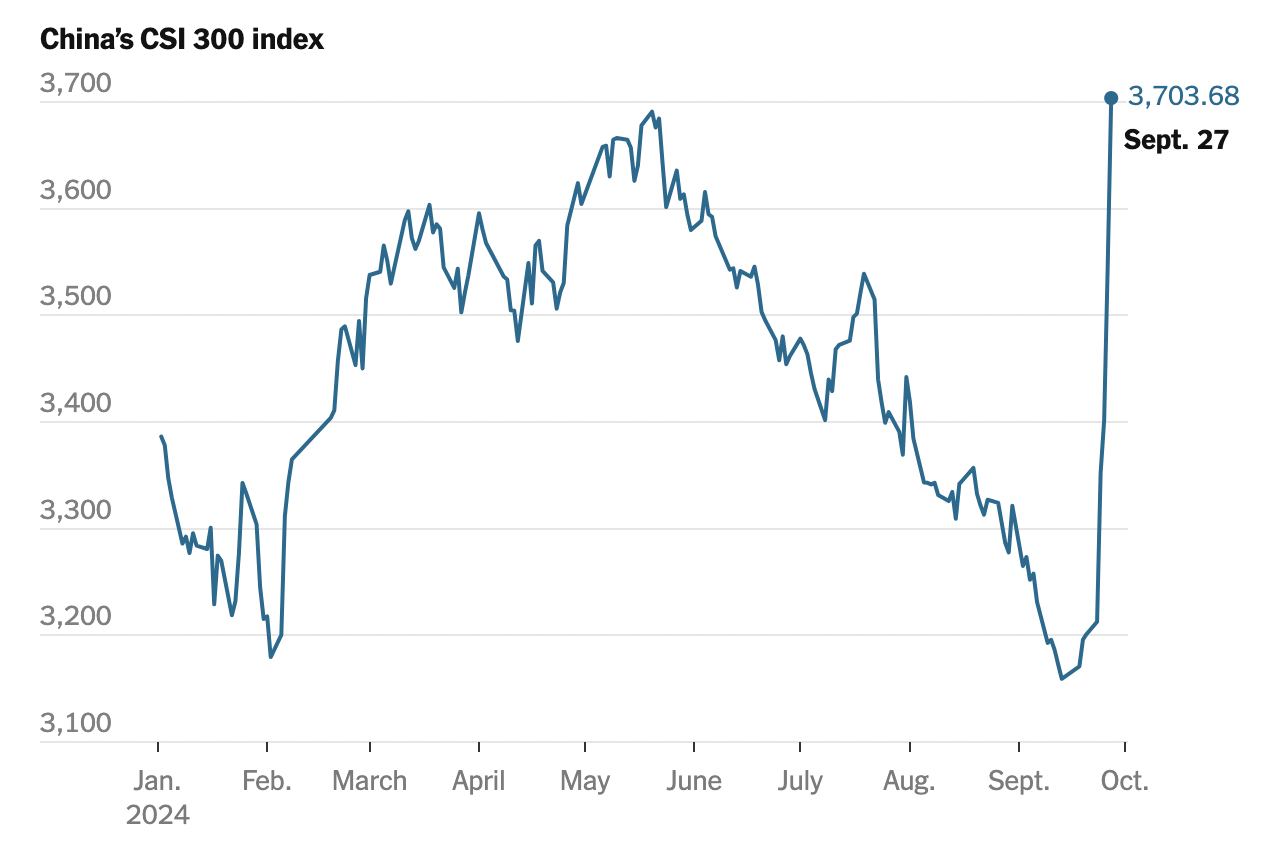

On the other hand, China’s recent monetary policy changes have caused their major indexes to rise considerably in the past few weeks. The Shanghai Stock Exchange (SSE) Index rose by almost 13% in the past business week after having fallen since May. Once again, however, these prices are being driven by macro news, which for equity markets, is speculation. There is no guarantee that China’s new monetary policy is actually going to help current financial constraints, nor that consumers will begin to support these high equity valuations by going out and buying goods and services.

Chart 2: CSI Index 2024 (Chinese Stock Performance)

What hit stock market enthusiasts this past week, however, was a Morgan Stanley call that effectively downgraded the entire US autos industry. Adam Jonas, Morgan Stanley’s Head of Global Autos & Shared Mobility Research downgraded names like General Motors, Ford, and Rivian. In a note released earlier this week, he cites a variety of reasons for this downgrade including the ongoing trade war with China, and the fact that Chinese alternatives are simply more user friendly. Surprisingly, he also slashed the price target for Tesla, his top pick, but more so in a move to show that the company is in a transitory period as it shifts from an auto company to an AI firm.

Based on these calls which spelled out a bad week for GM, Ford, and Rivian, we would also recommend offloading these stocks from your portfolio, as there seems to be no near term gain from holding this affected industry.

US Macro: I Have Midterms this Week and Thank God There Wasn’t Much News.

This week marks the first week I (Andrés) have not written the US Macro blurb first. Why? For all intensive purposes it has been a boring week in US macro. The effects of last week’s Fed decision are settling in, and with that, every day the Fed’s path becomes clearer (we’re not saying it is clear at all right now). As noted above, solid PCE numbers are currently solidifying a path for more rate cuts. We’ll have an idea about how aggressive the rate cutting cycle will be this coming Friday after the October Bureau of Labor Statistics report is released. Wall Street analysts are expecting a gradual cooling rather than a rapid slow-down, but honestly, who knows after COVID-19.

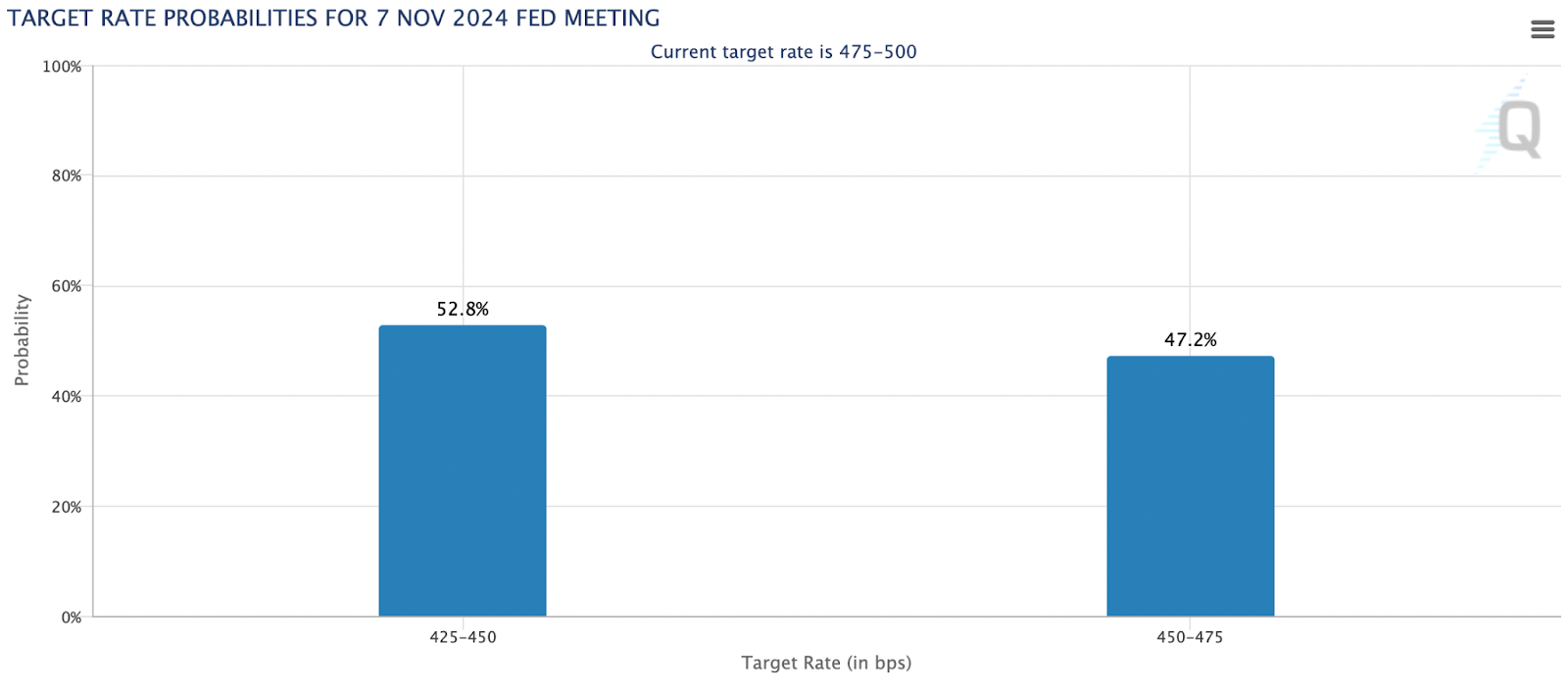

With the next Fed Meeting in 38 days, we still maintain our forecast for a 25 basis point cut in November. Most traders are pricing in a 50 basis point cut, but let’s see how this story develops in the coming month. Throughout this heavy speculation it may be in your interest to look at Treasury futures, seeing as predictions for lower yields will increase the prices of these contracts.

Chart 3: Rate Cut Probabilities by Market Makers

Check out the University of Michigan’s Survey of Consumers to see how confused and confident the average American consumer really is, and check out this report from the Bank of Canada regarding financial vulnerabilities. Spoiler alert, they’re concerned about housing. Obviously this is the US Macro section, but it is an interesting development to follow as our economies are closely aligned.

Global Macro: Rate Cuts… but for Oil!?

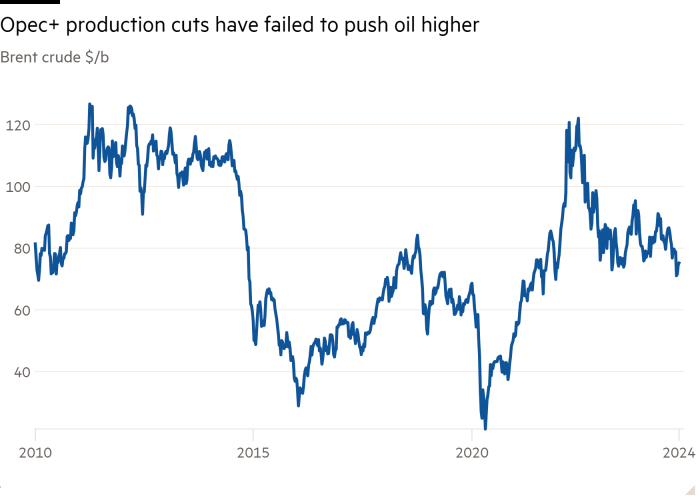

On Thursday, September 26th, Saudi Arabia decided to abandon their $100 a barrel price target for oil, in favor of higher production. This marks an extremely surprising piece of news, seeing as global demand has slumped, causing oil prices to fall since mid-2022. OPEC+, a consortium of oil-producing nations driving supply (and unofficially led by Saudi Arabia), was largely expected to cut supply this year to match slumping demand and drive prices higher. However, this development marks an end to the counter-cyclical supply shocks that historically allowed the OPEC+ cartel to drive prices to their liking.

Chart 4: Brent Crude Oil Prices per Barrel

There are many reasons why this shift occurred, mainly the growing role of the United States as a global producer of oil, which drives down the effect of collective OPEC+ supply. Hence, during the past two years as Saudi Arabia has led cuts in oil supply, prices have still fallen, because of the efforts of the United States to keep prices low amid geopolitical turbulence in Eastern Europe and the Middle East. In fact, after the onset of the Russia-Ukraine war, President Biden tapped into the US’s strategic petroleum reserves, purchasing over $180 million of barrels right after the conflict began. This was also done in an effort to curb inflation, which for American citizens, is tightly connected to oil prices.

Hence, as US supply has skyrocketed in the past few years, it has seemingly trumped the efforts of OPEC+ to reach the unofficial $100 a barrel price target. The end to counter-cyclical oil supply policy has huge ramifications when considering global economic and geopolitical conditions. Primarily, weakening demand for oil also helped drive prices down, and China, the second largest economy, has recently cut four important interest rates and pledged to spend enough to reach their 5% GDP growth target. The coinciding of these two changes, should prevent oil prices from falling too much, as these policies should stimulate demand for oil.

When looking at Russia: a nation at war, who is also a large producer of oil, this news is not too good. Oil is one of the main sources of revenue funding Russia’s war effort in Ukraine, and prolonged low oil prices are going to slow down the war effort from an economic standpoint. Furthermore, as Ukraine increasingly targets Russia’s oil and energy infrastructure, there could be major strains in Russia’s ability to fund their operations. When thinking about total market share of oil, as well, this does not bode well for the Eurasian nation. As Saudi Arabia is the second largest producer of oil, a commitment to increased supply can only mean an erosion in Russia’s oil revenue because any scarcity policy they pursue will be diluted by US and OPEC+ production.

While the United States is in the midst of trying to rebuild their oil reserves, this process has yet to make significant progress. Thus, using our supply and demand logic, we can expect Brent oil prices to hover around $70 a barrel for the near future.

Story of the Week: A Crash Course in Polling

Over recent months, national polling data has guided discourse surrounding this year’s presidential elections. While publishing giants like The Economist, The Washington Post, and The New York Times each publish well-renowned polling reports, polling information is not exclusively operated by legacy media. Instead, polling is a widely applied research methodology practiced at various firms, think tanks, and research institutions with differing motivations and goals.

With the intensity and complexity of this year’s elections, polling data has been at the forefront of commentary on both sides of the political spectrum and has dictated narratives throughout this election cycle. In this story of the week, we discuss the history of polling as a tool for political gauging, what methods comprise polling processes, and most importantly, if polling information is even viable for measuring the likelihood of election outcomes in light of its failures in past election cycles.

Modern political polling is characterized by precise hour-by-hour analysis that aims to calculate and continuously update likely election outcomes. While the earliest polling data of presidential elections in the United States involved straw polling in the 1840s, the basic method for modern polling was developed in the mid-1930s when the first public opinion polling agency was founded by political scientist George Gallup.

Using statistical methodologies including random and stratified sampling, Gallup and his team gained widespread notoriety for the accuracy of their methods. With the development of survey and mass communication technology since Gallup’s time, however, polling has evolved from its humble beginnings into a sprawling multi-billion dollar industry spanning research institutions, political parties, and think tanks.

These types of partnerships between polling firms and politicians have transformed modern political landscapes by providing real-time insights into public opinion, shaping campaign strategies, and influencing media coverage. Additionally, polling impacts policy decisions, as politicians often use it to assess public support for various initiatives.

In the context of Trump vs. Harris, collaboration between polling agencies and each campaign has directly influenced strategy throughout the race for the presidency. With influential think tanks like The Heritage Foundation and The Brookings Institute having access to detailed information gauging which issues matter most for target voting populations. This ease of access has raised concerns about the ethics surrounding the use of polling data and brought up intriguing questions about the integrity of political rhetoric in this year’s election.

Nonetheless, the accuracy and reliability of polls remain a topic of debate, especially given issues like nonresponse bias and inaccurate predictions in key elections. Even with the advancement of research and survey methodologies, polling can often still be a guessing game. With this upcoming election, polling is still a great indicator of the state of the race, but it is in no place to make a confident forecast for November’s winner.

Make sure to tune in next week for more market updates and global insights!