Preparing for the Trump Economy? Positioning Matters Most in a Complex Macro Environment

Authors: Andrés Larios, Sydney Sibrian, Faith Spalding

Story of the Week (Opinion): Tiara Nanayakkara

Editors: Venus Dhanda, Sydney Sibrian, Daniel Hou, Faith Spalding

Intro:

Welcome to the Weekly BluRB, a newsletter catered to students and professionals to get the latest news and insights on global markets. Get prepared for the week by reading four weekly stories circulating around equity markets, macro trends, geopolitics, and new business developments. And the best part: we’ll give you an informed view about where we think prices, policy, and trends are going in the near future. The content in these writings is for informational purposes only and does not constitute financial or investing advice.

Last Week’s Calls:

Buy PLTR: Up 43% (Woah)

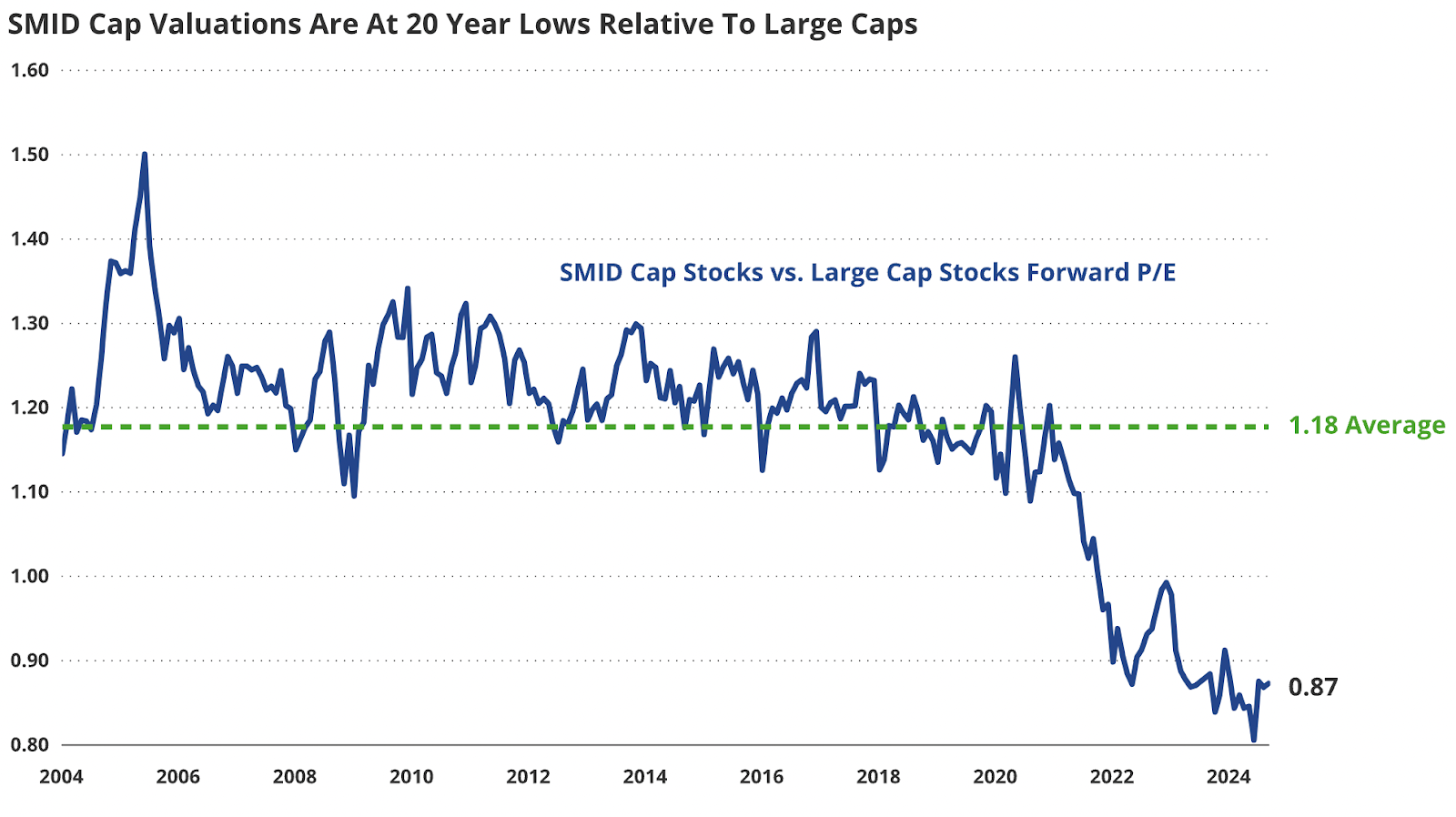

Buy SMID Caps: Russell 2000 up 10.17%

25 Basis Point Rate Cut: On Thursday, the FOMC cut by 25 basis points

Equity Markets: Trump’s Animal Spirits Rally The S&P 6000, Topple Volatility, Green Stocks

Last week’s presidential election triggered a strong market reaction following President-elect Trump’s historic victory. The S&P 500 opened on Wednesday morning 81.53 points higher than Tuesday’s market close. On Friday, the S&P 500 reached a staggering 6,000 points, a roughly 3.75% increase from the start of the week. Today (Monday), the S&P 500 closed above 6,000 points, reaffirming the market’s enthusiasm for Trump’s economic promises and so-called ‘Trump trades’.

The market rally wasn’t limited to large-cap stocks. The Russell 2000, our favorite indicator for small and mid-cap stocks, rose roughly 5.8% between Tuesday and Wednesday’s market close. Trump’s big promises for American businesses coupled with a declining interest rate environment bode well for SMID-cap stocks, which we note below are historically undervalued. These stocks appear well-positioned and poised to grow in the coming months. This underscores that it is not only the big players who anticipate reaping the benefits of Trumpian economics.

Chart 1: SMID Cap Valuations (Russell 2500) at 20 Year Lows Relative to Large Cap Stocks (S&P 500)

In other news, volatility may be taking a temporary backseat, in contrast to last week’s Volatility Index (VIX) call. The VIX is the stock market’s ‘fear gauge’, with VIX readings above 20 indicating market-wide uncertainty. Leading up to the election, the VIX soared as polls leading up to the election remained neck and neck, fueling fears of a prolonged or unresolved presidential outcome far beyond Election Day. However, with Fox News calling the election at 10:50 pm PST, Trump’s decisive victory led investors to pivot towards stocks that surged under Trump’s first presidency, notably small caps and the financials, tech, and energy sectors.

That said, it’s still too early to declare victory against market volatility. Trump’s proposed tariff policies are likely to cause drastic short-term disruptions not only in global markets, but also domestically. While equity markets appear poised for strong growth through January (ahead of Trump’s inauguration), his ambitious economic policies raise many questions about their feasibility. Building the manufacturing-intensive infrastructure to support his America First economic proposals will take time and most likely will put immediate pressure on the purchasing power of American consumers’.

Chart 2: CBOE’s Volatility Index Drops by Roughly 32% Following Trump’s Victory

Amid last Tuesday’s election results, green investors are fearful for the future of renewables and climate action. The COP29 climate summit is set to kick off in Baku today and the U.S.’s absence doesn’t exactly come as a surprise given the current landscape. Trump’s ‘red wave’ triggered major solar and wind sell-offs, with share prices of renewable energy stocks plummeting. Among the most affected were Enphase Energy, down over 20%, and Sunnova, plunged a staggering 46%. Enphase has already announced layoffs in the coming months. The president-elect plans to roll back several climate reforms implemented by the Biden administration, setting the stage for long term fluctuations in sustainable markets, notably by taking aim at the Inflation Reduction Act.

The Inflation Reduction Act (IRA), signed into law by President Biden in 2022, fused climate and industrial policy by imposing stricter emission standards, with the aim of reducing inflationary pressures and costs. Trump intends to overhaul the act and rescind any unspent funds. This includes getting rid of the 45x Advanced Manufacturing Production Credit which enables companies to receive production tax credits for solar, wind, and battery components. Without these credits, renewable energy projects become less financially viable. While many believe that domestic infrastructure for renewable companies is strong enough to withstand the looming challenges, a Republican majority in both houses of Congress is poised to deliver deregulatory policies that undermine the sector’s competitive advantage, slowing the American transition to clean energy.

US Macro: Is Jerome Powell Unfireable? And Rationalizing our December FOMC Call

VICTORIA GUIDA: Some of the president-elect’s advisors have suggested that you should resign. If he asked you to leave, would you go?

CHAIR POWELL: No.

VICTORIA GUIDA: Can you follow up on—do you think that legally you’re not required to leave?

CHAIR POWELL: No.

On Thursday, the FOMC decided to cut interest rates by 25 basis points, lowering the target range to 4.50-4.75%. This was the most likely outcome, with markets expecting nearly a 100% chance of this happening. However, what made headlines was Fed Chair Jerome Powell’s comments during his press conference. After beginning his tenure as Fed Chairman in 2018, Jay Powell and Trump have butted heads on numerous occasions, with Trump expressing his desire to exert control over the Federal Reserve, an independent government body.

Following Chair Powell’s short but stern answers on Thursday, it was clear that the FOMC has been thinking about the ramifications of a second Trump presidency on monetary policy and Fed independence, with reports that the Federal Reserve is even prepared for a legal battle. Embarking on a political crusade to end Fed Independence is a tall task that won’t sit well with the stability of markets. IMF Chief Economist and Berkeley professor (Go Bears!) Pierre-Olivier Gourinchas calls Fed Independence “one of the great accomplishments that we’ve had over the last 50 years.” The Trump administration’s proposal of high tariffs, mass deportation of undocumented agricultural workers, and (many) tax cuts, are sure to enact high inflationary pressures, urging the Fed to reconsider its rate-cutting plan.

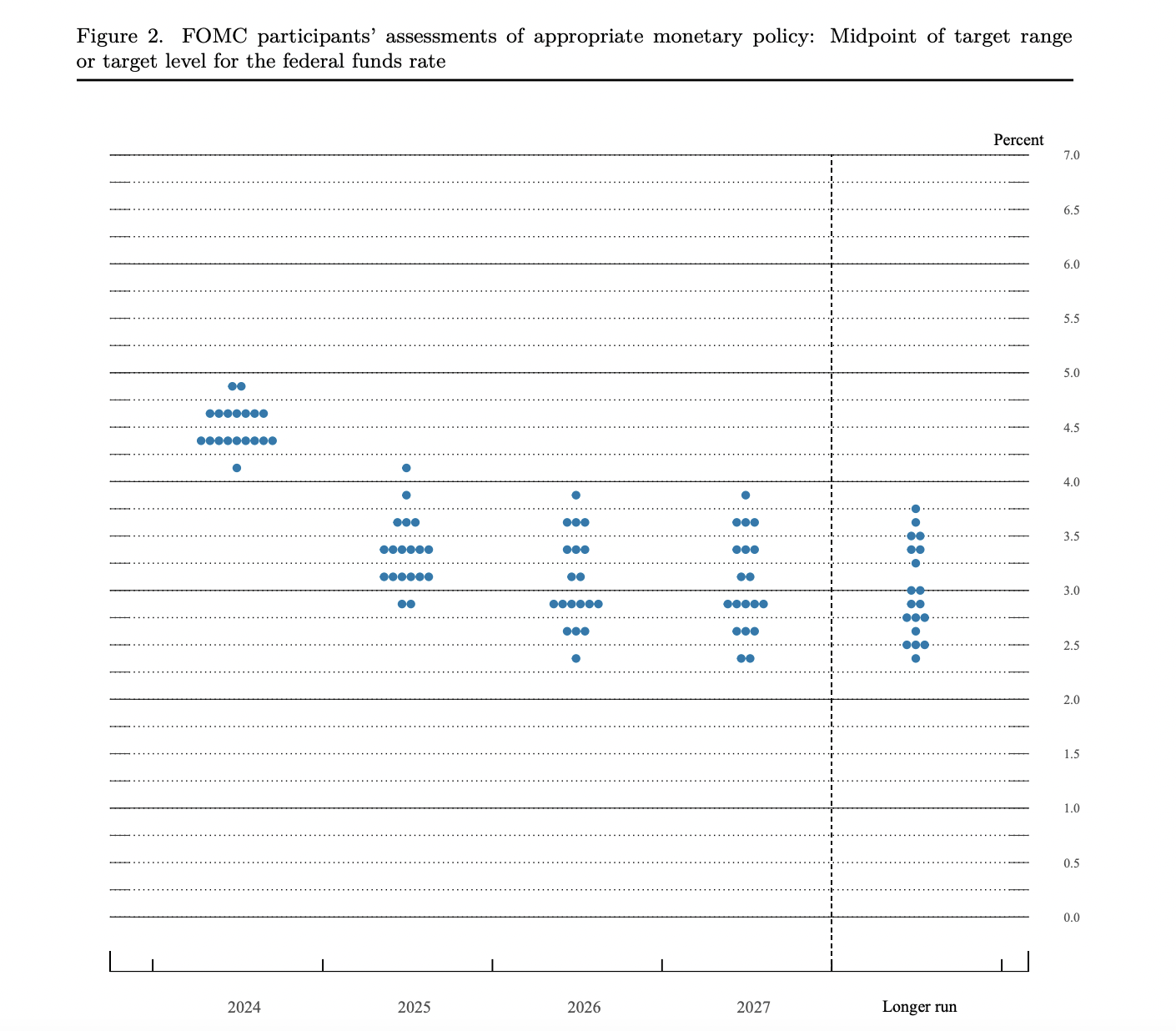

With regards to the FOMC’s policy plan moving forward, Thursday’s press conference provided many hints about December’s meeting, though it remains a tricky meeting to predict. With important data like the NFIB Optimism Survey, a CPI and PPI print, and jobless claims all being released this week, we’ll have a lot to discuss in next week’s Weekly BluRB. As of today, however, we are predicting that the Fed will keep the Fed Funds Rate at its current target range. By analyzing September’s FOMC projections for the Fed Funds Rate level at the end of 2024, we can see that 9 FOMC members predicted the Fed Funds Rate to remain above 4.5%, with 10 members predicting the rate to go lower. This displayed a real lack of consensus to end the third-quarter of 2024.

Chart 3: FOMC Participants’ Projections for Fed Funds Target Range

The Fed has received much criticism due to its seemingly excessive dependence on data, reacting to weekly prints rather than overall trends. Thus, many believed the Fed should have started cutting in July by 25 basis points, to avoid a 50 basis point cut in September, with many citing the Fed being ‘behind the yield curve’. Following September’s rate cut, employment data continued to cool, though not as quickly as initially anticipated. With Governor Michelle Bowman’s historic dissent for the September rate cut and Governor Waller’s acknowledgement of a really resilient economy, we believe the Fed was positioning itself as more hawkish, regardless of the President-elect.

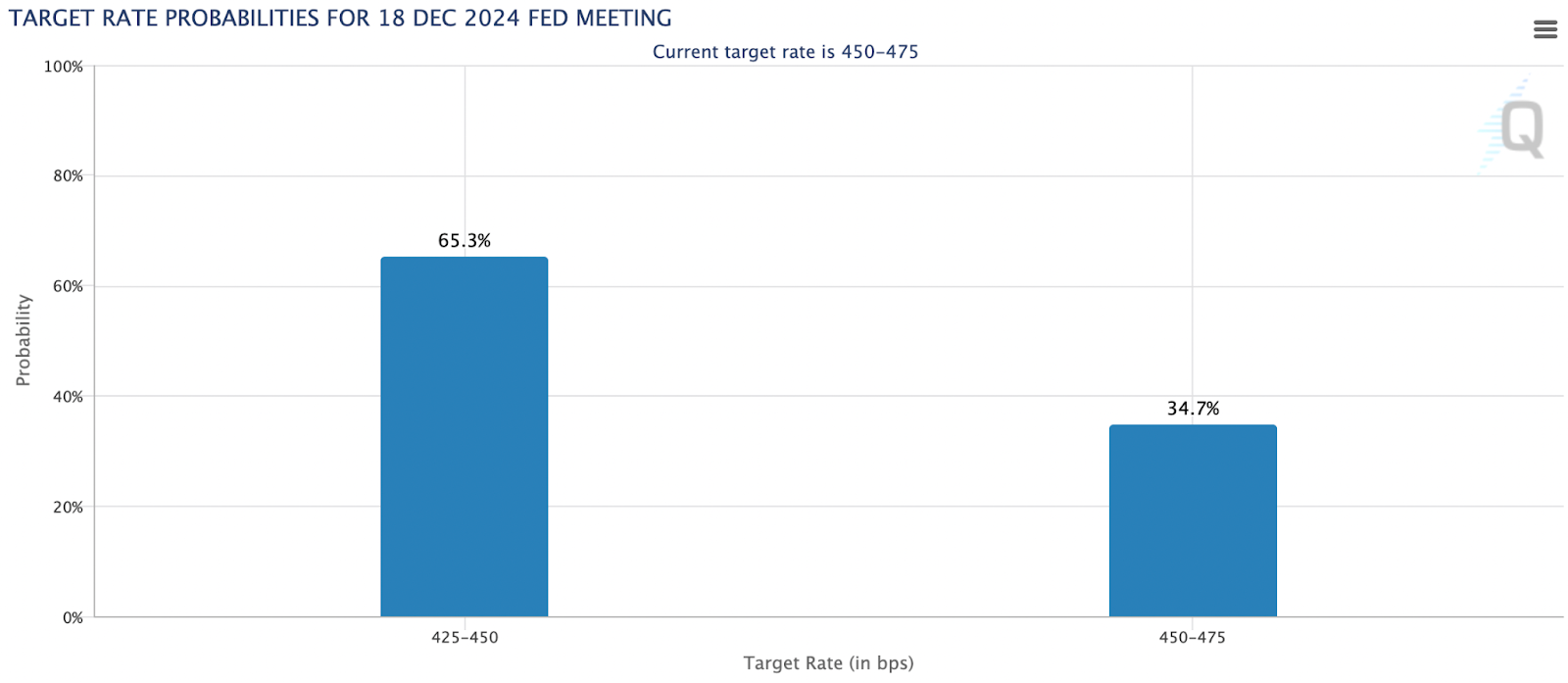

Chart 4: Market Probabilities for December Fed Meeting show 25 BP Cut Expected

With Trump set to assume office on January 20th, 2025, we believe the Fed will begin to position itself to counteract the inflationary pressures from Trumpian policies noted above. When asked about a rate hike in 2025, Chair Powell answered:

“I wouldn’t rule anything out in that far away. But that’s certainly not our plan. I mean, our baseline expectation is that we’ll continue to move gradually down towards neutral, that the economy will continue to grow at a healthy clip, and that the labor market will remain strong.”

It’s pretty clear from this language that Chair Powell does not want to increase rates any more, so it is in our view (in contrast to market probabilities in Chart 4) that with the new data coming in this week, we will see statistics that supports a resilient economy and the inflation rate moving closely to the 2% target rate. In the event of this base case, it would be prudent to keep rates at their current level, for a total of 75 basis points cut in 2024 to ensure the Federal Reserve’s dual mandate and proper positioning for the next four years.

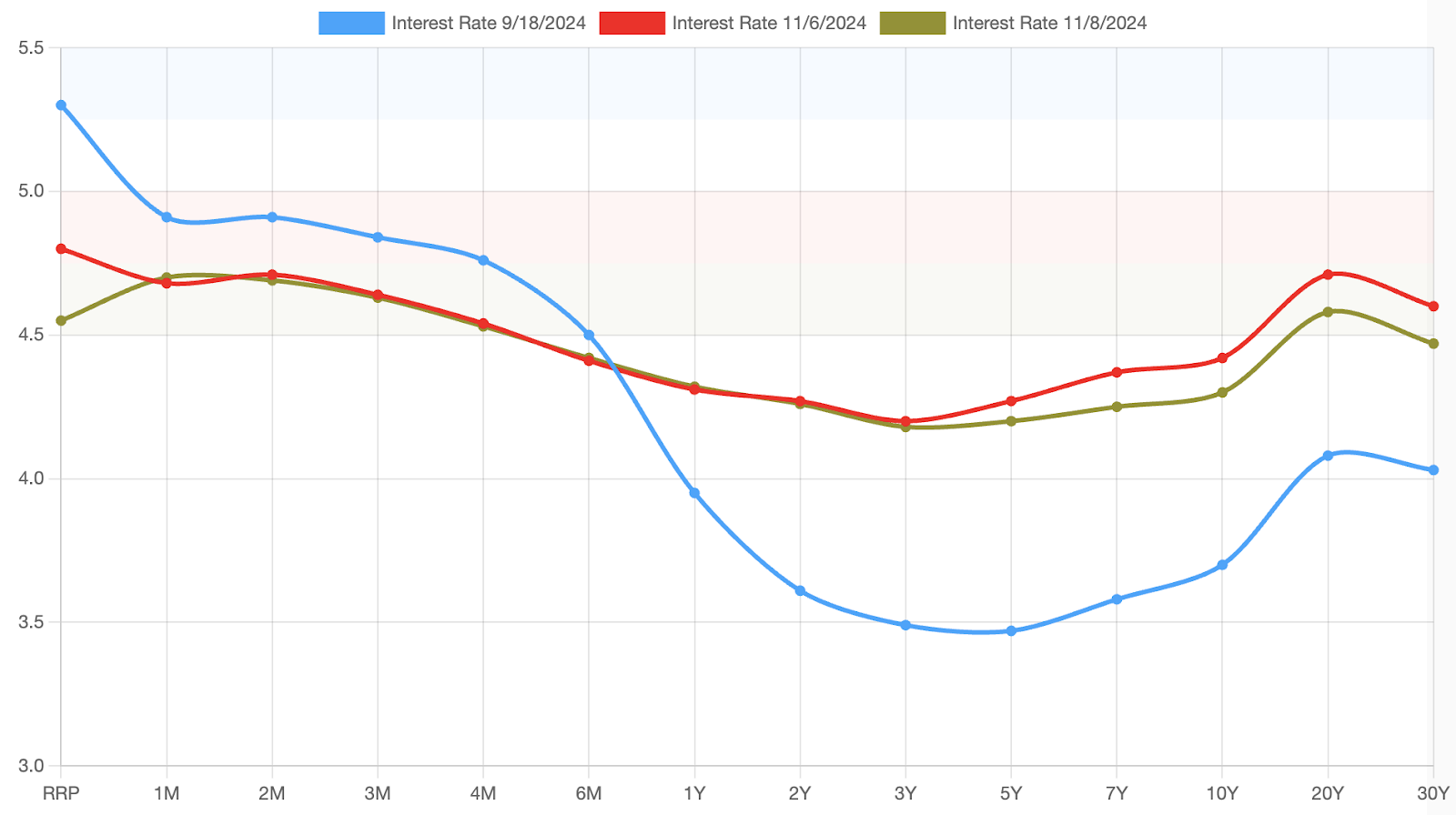

Chart 5: Long Term Rates Drop Slightly, Following November’s Rate Cut.

Following Thursday’s rate cut, long term yields fell by roughly 10 basis points (Chart 5). All in all, it’s still expensive to borrow, and these high yields will impact American businesses and consumers alike. The shape of the yield curve will become increasingly important during the Trump presidency, seeing as it is unlikely for nominal rates to reach zero. By continuing in a high interest rate environment to combat inflationary pressures, the high rates at the back-end of the yield curve should be a major concern for policymakers. Taking note of the Federal Reserve’s balance sheet composition and size may help us predict how the back-end of the yield curve may change over time.

Global Macro: Europe’s Woes and China’s Lows

Europe:

Last week, we declared Europe to be the big losers regardless of the U.S. presidential election outcome. Following Trump’s victory on Tuesday, Europe is set to have to deal with at least four years of their perceived worst outcome. With deep structural economic problems, the threat of American tariffs and American repercussions for further engaging in trade with China, as well as their inability to stop funding Russia’s war machine through energy infrastructure and consumption, it seems as if Europe has dug itself into a very deep hole. Although Russian President Vladimir Putin and President-elect Trump have spoken on the phone with regards to the Russia-Ukraine war, Ukraine still seems to be holding the short-end of the stick among all EU, NATO, and allied nations.

Germany’s (Europe’s de-facto leader) ruling coalition (and hence their government) collapsed last week, as German Chancellor Olaf Scholz fired his Finance Minister Christian Lindner. Scholz is a member of the left-leaning Social Democratic Party (SDP), while Lindner represents the fiscally conservative Free Democrats Party (FDP). These two parties formed a coalition in the German government (along with the Green Party) aimed at halting far right rhetoric in the nation, claiming to be a ‘traffic light coalition’. Following Lindner’s sacking, the FDP withdrew from the coalition, leaving Germany with no majority body and a fragmented government. With a Vote of Confidence set to be held in Parliament before January, Germany’s political risk will surely reverberate across Europe.

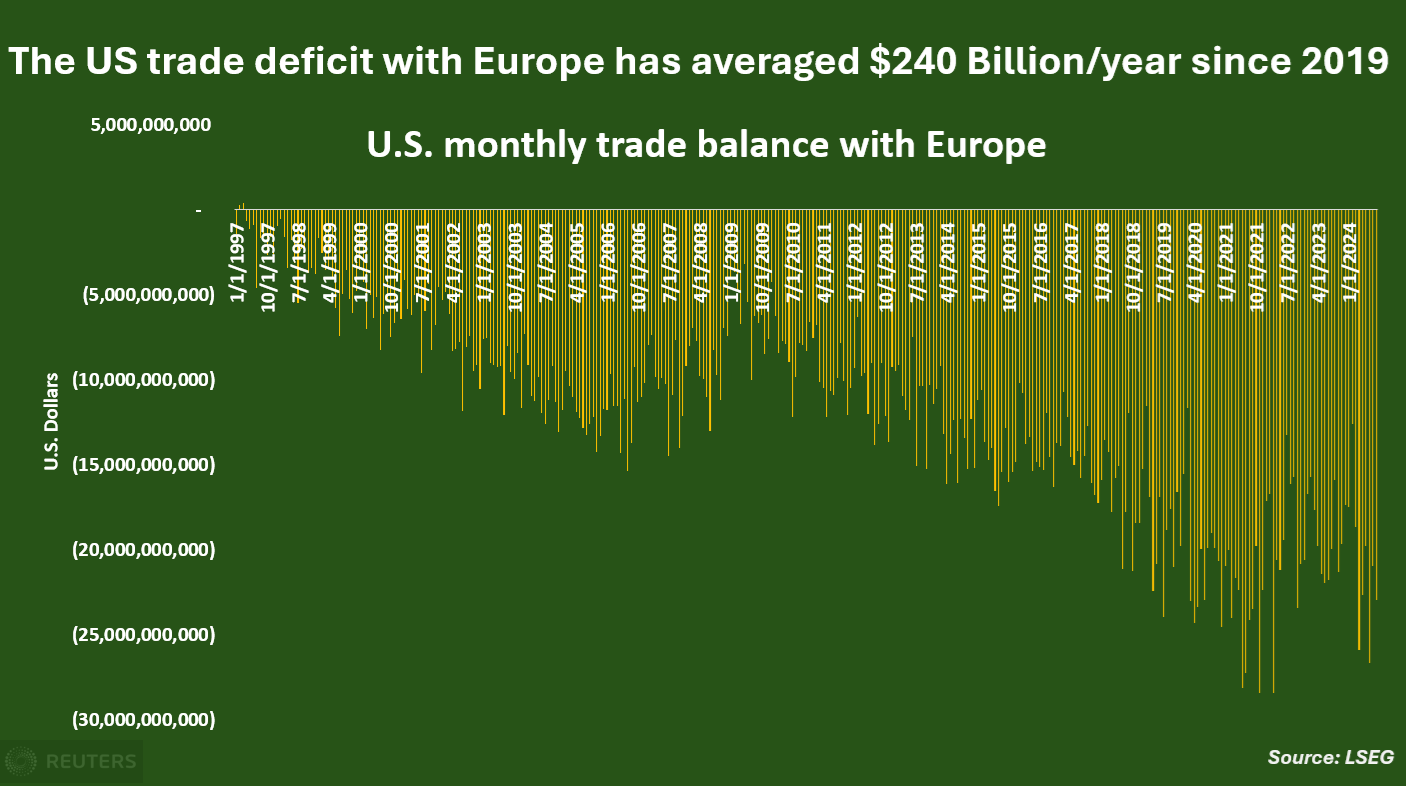

Furthermore, the threat of Trump tariffs looms over European markets, with ING Bank saying his tariffs could even cause a recession. With a proposed 10% blanket tariff on all imported goods, and the United States’ being Europe’s biggest trade partner, we could see severe strains on the Eurozone economy. Trump has looked at European countries as a hindrance seeing as the U.S.-Europe trade deficit has increased markedly over the course of the 21st century (Chart 6). Trump’s European tariff policy would aim to profit from Europe’s stagnation as a trade partner by increasing government revenue from imports.

Chart 6: U.S. Trade Deficit has Increased as Europe’s Economic Growth has slowed.

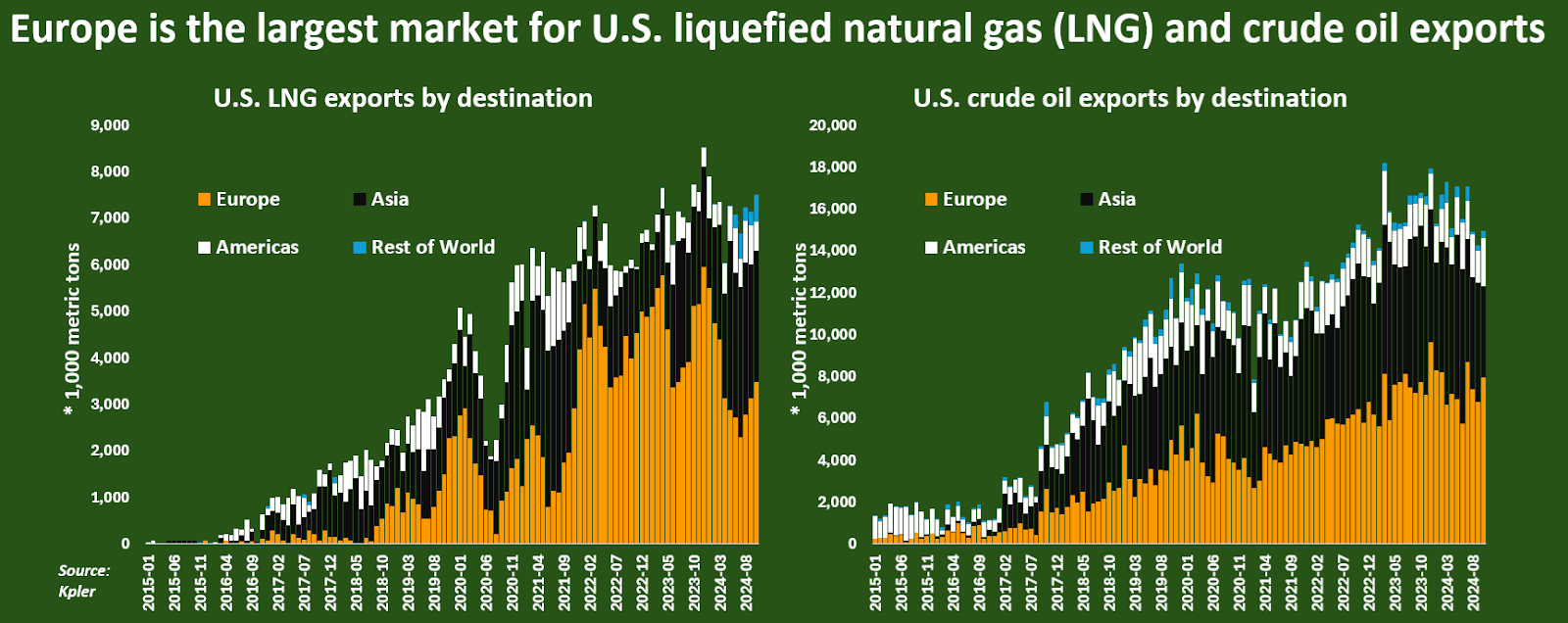

Despite this mounting trade deficit, Europe is the biggest market for American energy exports. Following the beginning of the Russia-Ukraine War, the United States has stepped up its natural gas and crude oil supply to Europe. Even so, before the Russia-Ukraine war, Russia supplied Western Europe with 40% of its natural gas. Individual European countries have implemented mixed policies surrounding Russian energy imports, seeing as U.S. products are largely more expensive. This shows Europe’s energy dependence on Russia, and a lack of a coordinated economic plan to hinder Putin’s war machine.

Chart 7: Following Russia-Ukraine War, Europe Has Stepped Up as the U.S’ Main Energy Importer

Ultimately, Trump’s victory, coupled with Germany’s government collapse, shows that Europe has lagged behind other developed nations, while also failing to prepare for a Trump presidency. This could spell out poor or even negative Eurozone economic growth, severe compromises to end the Russia-Ukraine war, and possible political uncertainty as the European population reacts to reduced standards of living with extremist politics.

China:

Several weeks ago, we reported on China’s monetary easing policies to stimulate short term growth amidst Chinese economic shortcomings. Now, Beijing announced a series of fiscal stimulus packages in the form of 10 million yuan or $1.4 trillion in debt swaps on Friday, facing fresh pressure as the reelection of U.S. President-elect Donald Trump reignites fears of escalated trading tensions with propositions for a 60% tariff increase. These ‘debt swaps’ are a financial restructuring mechanism where existing ‘shadow’ debt (debt between municipal and federal government) is refinanced at no extra cost.

In China’s case, this is a pivot towards local government stimulus, where local governments debt quotas are set to increase by 6 trillion yuan over the next three years, while the new funds will repay “hidden debts”, or government loans, bonds, and other shadow credits of local government financing vehicles (LGFV’s). While these policies may reduce local governments’ debt and interest burdens, economists speculate this will still not be enough for sustained progress needed to boost the ailing economy, as there’s an absence of direct stimulus measures combined with continued fears of a slow-growth rut and an escalated trade war. With that being said, there is still speculation that China has saved the best for last, with more fiscal stimulus reportedly in the works.

Story of the Week (Opinion): Economy Over Rhetoric – How Trump Won the Latino Vote

It was the election of our discontent–well, not entirely. Despite President-elect Donald Trump’s negative rhetoric towards the Latin American community, exit polls showed an increase in Latino voters, specifically males, voting for Trump in this year’s 2024 Presidential Election. During his failed 2020 campaign, only 36% of Latino men voted in favor of Trump while more than 50% voted in support of Joe Biden. With regards to Latino women, 70% had voted for Biden, leaving only 30% in favor of Trump in 2020.

However, this election year did not fail to entertain with a series of tumultuous surprises: Donald Trump promising revenge against his opponents, Biden dropping out three months before election day, and, even worse, comedian and Trump supporter Tony Hinchcliffe referring to Puerto Rico–a U.S. territory–as a ‘floating island of garbage’ only a week before the election. Despite all this, a little over fifty percent of Latino men still voted for Donald Trump while 38% of Latina women also voted in his favor. But why?

Some find it hard to conceptualize how Trump garnered such strong support from the very demographic he has insulted since the beginning of his 2016 campaign. However, many Trump supporters–former and unprecedented–were motivated by one key element: improving the American economy. It is no surprise that President Trump prides himself on creating the “best economy in the world” and yet, some economists are fearing the worst for the economy under another Trump term. During his presidency, The National Bureau of Economic Research noted how his “accomplished” tariffs actually led to an increase in higher prices for household items, imports, and machinery overall. Despite this, Trump hopes to establish tariffs on all goods imported into the U.S. to encourage domestic production, which some economists believe will only make goods more expensive and further harm the economy.

Tariffs aside, Trump has also boasted about his eagerness to execute “the largest deportation in the history of our country,” targeting undocumented immigrants, who are largely from Central American nations. Interestingly enough, this comment did not hinder much of the favor he possesses over Latino voters–if anything, some evidence suggests that certain Latinos were in favor of enforcing the Mexican-American border and establishing stricter regulations on immigration as a whole. Although the situational irony seems to be the most concerning factor, economists and business groups alike have warned that the deportation of millions of immigrants would place the American economy in a very vulnerable position because of the nation’s reliance on cheap immigrant labor, specifically in the agricultural sector. Immigrants are known to contribute greatly to the American economy, by filling in labor shortages at significantly lower costs.

Regardless, Latino voters contributed greatly to the re-election of Donald Trump. Despite the documented accounts of Trump targeting Hispanics in all three of his campaigns, Kamala Harris’s campaign message did not sufficiently move the Latino community. As a whole, the Latino vote is not a simple endorsement, especially when taking into account its constituents of diverse countries and complex regional histories. The Democratic party relied heavily on the right wing’s disturbing rhetoric to deter Latino voters, but it was not enough. Evidently, Latino voters wanted clarity from their presidential candidate for a prosperous economic vision, which Trump was able to readily supply. It appears Trump’s promises for a better economy was enough for Latino voters to overlook his consistent marginalization and cast their vote for him, possibly tipping the election in his favor.

Make sure to tune in next week for more market updates and global insights!