Elections and Rejections: All Eyes on The United States Following a Turbulent October

Authors: Andrés Larios, Venus Dhanda, Faith Spalding

Editors: Venus Dhanda, Sydney Sibrian, Faith Spalding

Intro:

Welcome to the Weekly BluRB, a newsletter catered to students and professionals to get the latest news and insights on global markets. Get prepared for the week by reading four weekly stories circulating around equity markets, macro trends, geopolitics, and new business developments. And the best part: we’ll give you an informed view about where we think prices, policy, and trends are going in the near future. The content in these writings is for informational purposes only and does not constitute financial or investing advice.

Equity Markets: Volatility is Incoming and Here to Stay: How to Navigate Equities in a Noisy Election

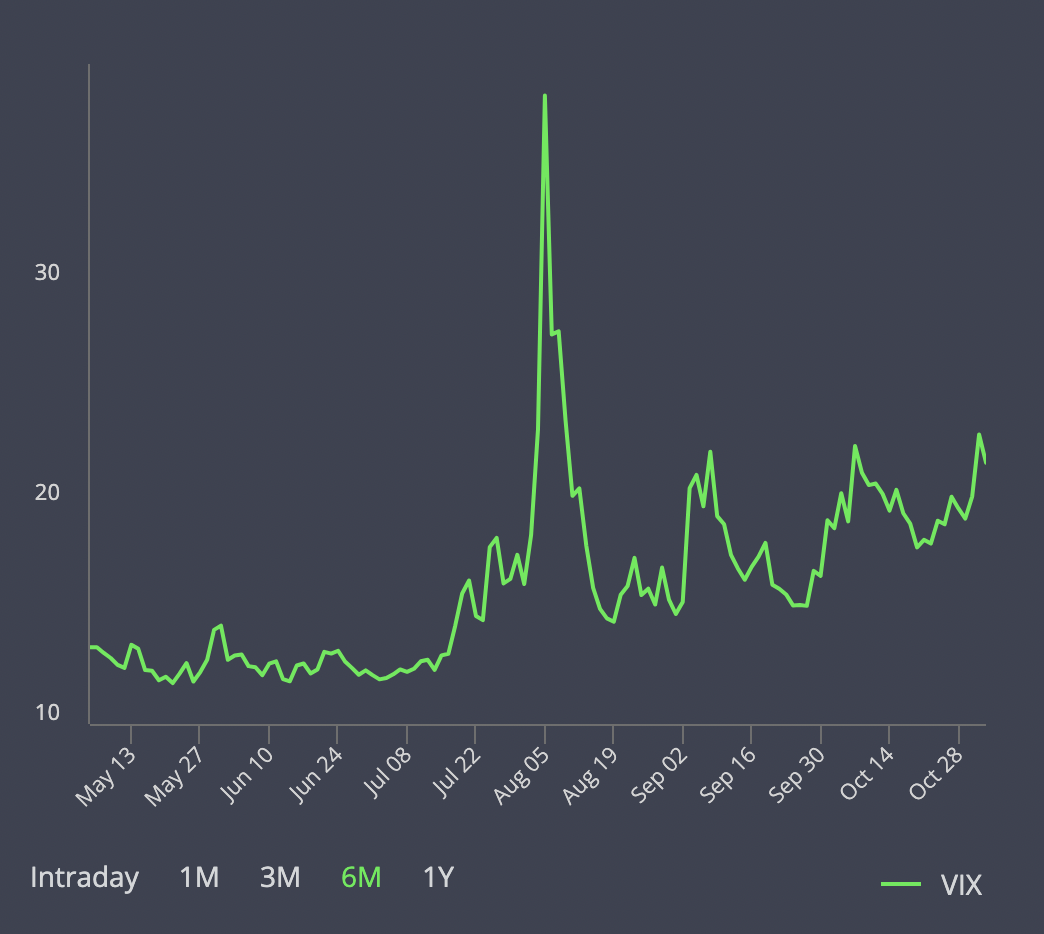

With just two more days left before a highly consequential U.S. presidential election, all eyes are on the stock market. Just kidding, but in this section, we will go over how the stock market can give us hints into not only how the election will pan out, but how the economy will fare in the days following November 5th. All in all, Wall Street isn’t betting on a specific candidate, but they are definitely making bets on volatility. The Chicago Board Options Exchange’s infamous volatility index (VIX), which measures anticipated market turbulence, surged 34% in October, the third-highest increase pre-election spike on record. This jumps suggests uncertainty is here to stay. Current polls show Vice-President Harris with a narrow lead over Former President Trump, while betting markets favor Trump, raising the likelihood of an unresolved outcome well past election night.

Chart 1: Volatility Index in Past Six Months

Outside of politics, the Federal Open Market Committee (FOMC) is set to meet on November 6th and 7th, with traders overwhelmingly expecting a 25 basis point rate cut. Meanwhile, big tech earnings have been a mixed bag and the S&P 500 fell by 105 points last week, its first weekly loss in five months. But there’s still more earnings to come that will help us gauge how industry is faring in new market conditions. Amid these uncertain times, we believe it is crucial to focus on company fundamentals and consider the impacts of potential economic or geopolitical shifts on stocks under each election outcome.

As we’ll elaborate on in the US Macro section, the entire yield curve seems to be rising with higher long term inflation expectations due to both candidates proposing spending-heavy economic plans. But the yield curve doesn’t just reflect bond market dynamics — it is a gauge for future economic conditions, incorporating inflation expectations from investors. Hence, Goldman Sachs predicts that S&P 500 returns may annualize just 3% over the next ten years, a sharp contrast from the 2014-2024 13% average. With large-cap stocks dominating headlines over the past 10 years, it is now more important than ever to look at mid-cap or small-cap stocks, while also considering other asset classes (depending on your risk profile) like Bitcoin and Gold, which are outperforming the S&P 500’s already impressive 2024 returns.

In contrast to what we just said about large-cap stocks, we are continuously bullish on one S&P 500 name which seems election-proof. In the year leading up to the election, large-cap stock Palantir Technologies (PLTR) has risen more than 144%. PLTR serves mostly governmental and commercial clientele, with unbridled demand in both sectors rising as a result of its AI platform. Its landing of a major Department of Defense contract underscores the national dependence on the company. If the election yields a Trump victory, projected defense spending will remain high and reduced business regulations will aid in maintaining its strength. In the case of a Harris victory, although she has not laid out a structured Defense policy outline, we can rest assured that Palantir’s strong balance sheet and involvement in the Middle East conflict will continue to drive client demand. Set to release its Q3 earnings report on Monday, analysts predict a revenue climb of 26% and EPS growth of 29%. With good fundamentals and a great outlook, PLTR presents an attractive investment opportunity no matter the victor on Tuesday.

US Macro: Jobs Report, Political Ammunition, and We’re (Literally) 99.9% Sure We’re Getting our Fed Call Right

Last Friday, the Bureau of Labor Statistics released its latest employment report for the month of October, and political analysts are torn on what this means for the upcoming presidential election. This report comes at a crucial time for the American public as it is the last large piece of economic data before the presidential vote. The economy is a major factor for all in this election, especially undecided voters. And with a Democrat leaving the presidential office, it also presents former President Trump with ammunition against his Democratic opponent, which he recently used at a rally on Saturday in North Carolina, calling the report “Depression-type numbers”.

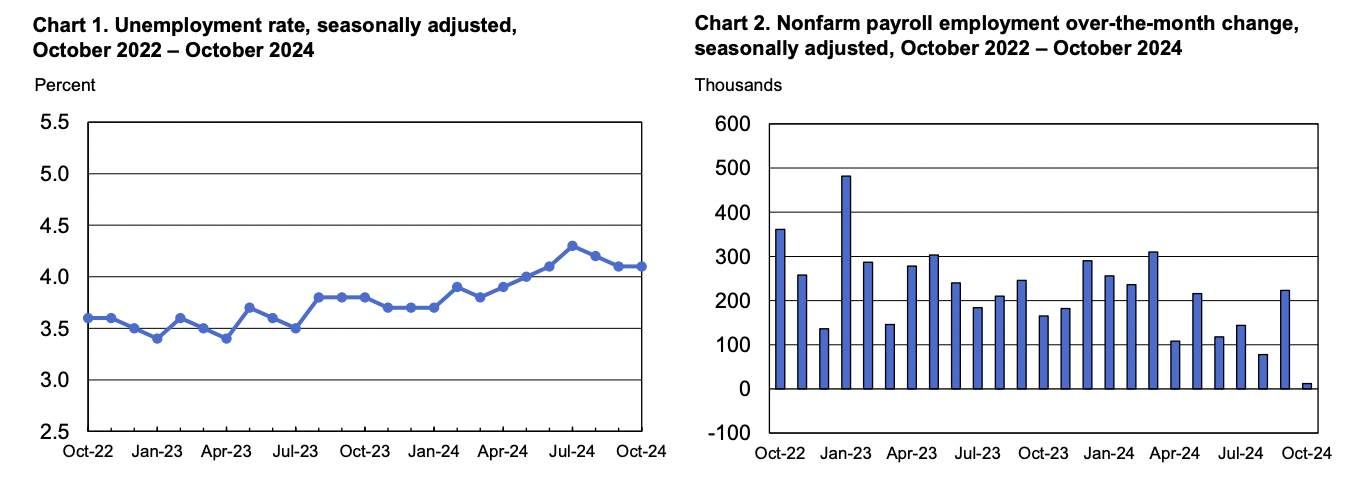

The jobs report showed a drastically slower increase in employment with only 12,000 jobs added in October, far below expert estimates and the lowest number since December 2020. Unemployment remains constant at 4.1%, and average hourly earnings increased 0.4%. However, the BLS notes the large negative impact of two disastrous hurricanes (and ensuing measurement difficulties) and a large labor strike against Boeing in this short timespan. The Boeing union protests put a hold on 44,000 jobs in manufacturing, a sector that had 46,000 jobs depleted in total. These jobs are expected to reappear in the economy (and its subsequent jobs report), but the manufacturing industry has been lacking numbers in this past year, only adding jobs in 4 out of the 10 months.

“The big one-off shocks that struck the economy in October make it impossible to know whether the job market was changing direction in the month,” comments economist Bill Adams at Comerica Bank. Large numbers of American voters have expressed their discontent with the recent state of the economy (despite its strength), and this report has only encouraged similar sentiment to grow, especially among republicans.

Chart 2: Although October saw U.S. employers only add 12,000 jobs, the unemployment rate remained steady at 4.1%

Despite this hectic jobs report, it is important to contextualize the data not only with strikes, natural disasters and the election, but also within the United States’ broader economy to predict how the Federal Reserve may react on Thursday’s meeting. Chart 2 is important because it shows that this October was an anomalous month in terms of job gains, yet despite everything, the unemployment rate remained constant. Even though the labor market does seem to be cooling (which is why the Fed is cutting rates), it isn’t cooling as quickly as previously thought. Traders are pricing in a 99.9% chance of a 25 basis point rate cut (at the time of publication), in line with our view.

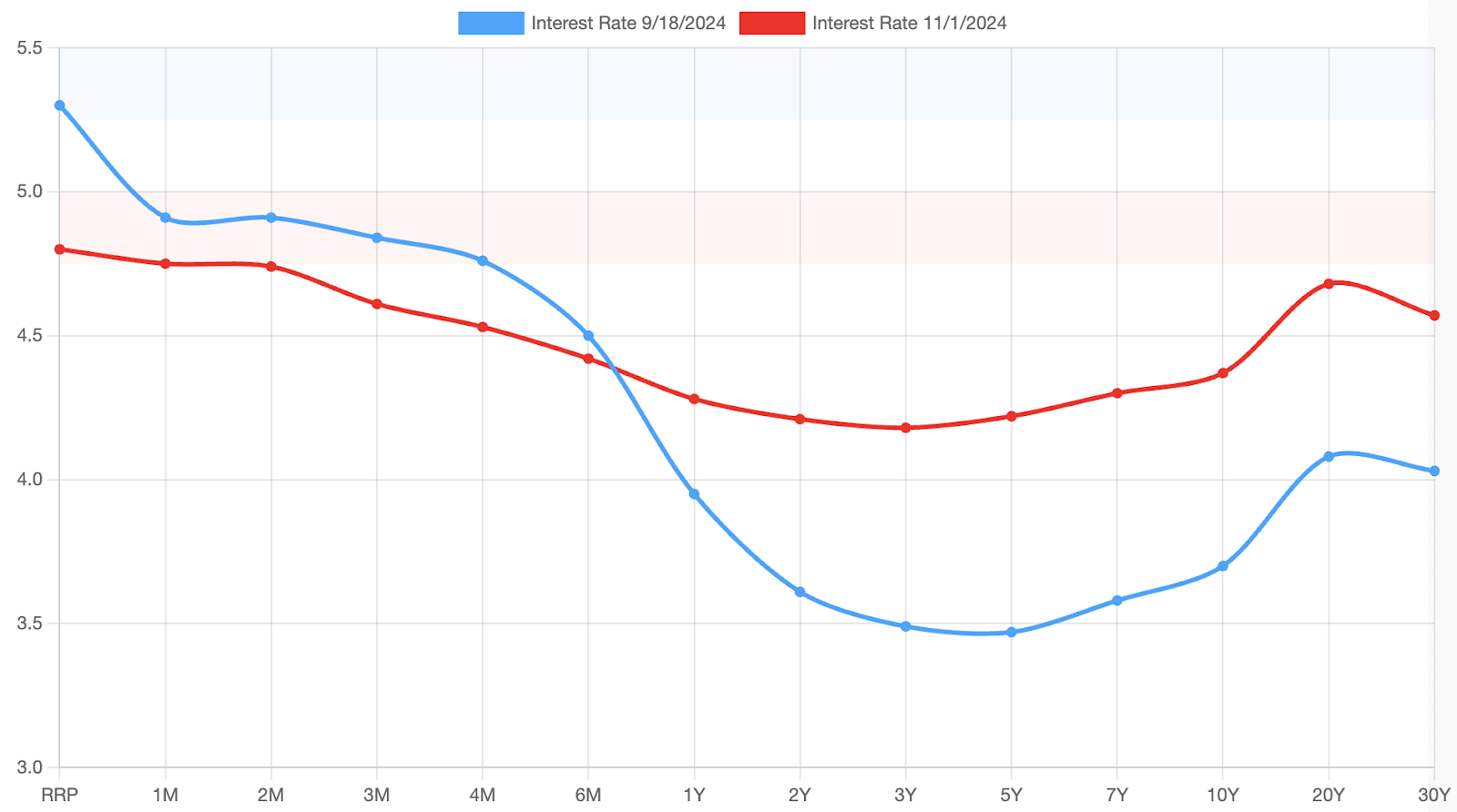

While inflation has definitely not been completely beaten, it is also expected to return due to Presidential candidate’s Trump and Harris’ promises to keep spending without addressing the national debt. As noted in our equity section, the yield curve is rising rapidly, and although it has dis-inverted and is flattening, it is becoming increasingly expensive to borrow.

Chart 3: US Treasury Yield Curve on Day of September Rate Cut vs. Last Trading Day

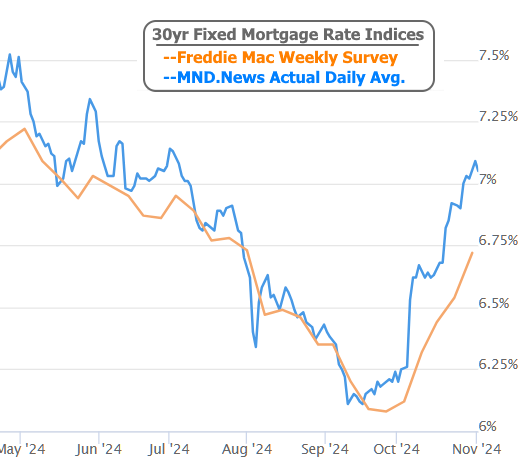

Although short term borrowing is cheaper today than it was a month and a half ago, long-term borrowing is now around 50-70 basis points more expensive. While a flattening of the yield curve is expected after a rate cut, the quick rate in which this happened shows investors fears of uncertainty and high inflation in the future due to Tuesday’s presidential election. In more practical terms for the US consumer, interest rates, and hence mortgage rates have inched up following the Fed’s 50 basis point cut. This means that although the short-term interest rate environment is more easy, it is becoming increasingly more difficult for Americans to make big investments like buying a home or a car, due to this yield curve phenomenon. We can expect higher delinquency rate data in the near future.

Chart 4: Mortgage Rates have inched upward after September rate cut

Fed independence isn’t expected to be as big of a deal as thought leading up to the election, however, the long-term economic outlook for the United States is still up for grabs, not only domestically, but in terms of international trade, foreign exchange, and economic superiority. Learn more in our global macro section.

Global Macro: Risky Business – The Election and its Global Market Ramifications

Breaking News: The United States is still the most important country in the world, and Tuesday’s presidential election is major proof. We see foreign exchange rates becoming more volatile through political risk and differing policy cycles between the Federal Reserve and the Bank of Japan, as well as fears of increased tariffs on China, especially as a result of a possible Trump victory. Seeing as market’s are pricing in high inflation risk through Treasury yield curves, there is no doubt there will be spillovers in other developed markets like Europe due to strong economic linkages. One thing is certain, however; this Presidential election has consequential global economic outcomes, and market forecasters are predicting upside inflation risk regardless of who becomes President-elect.

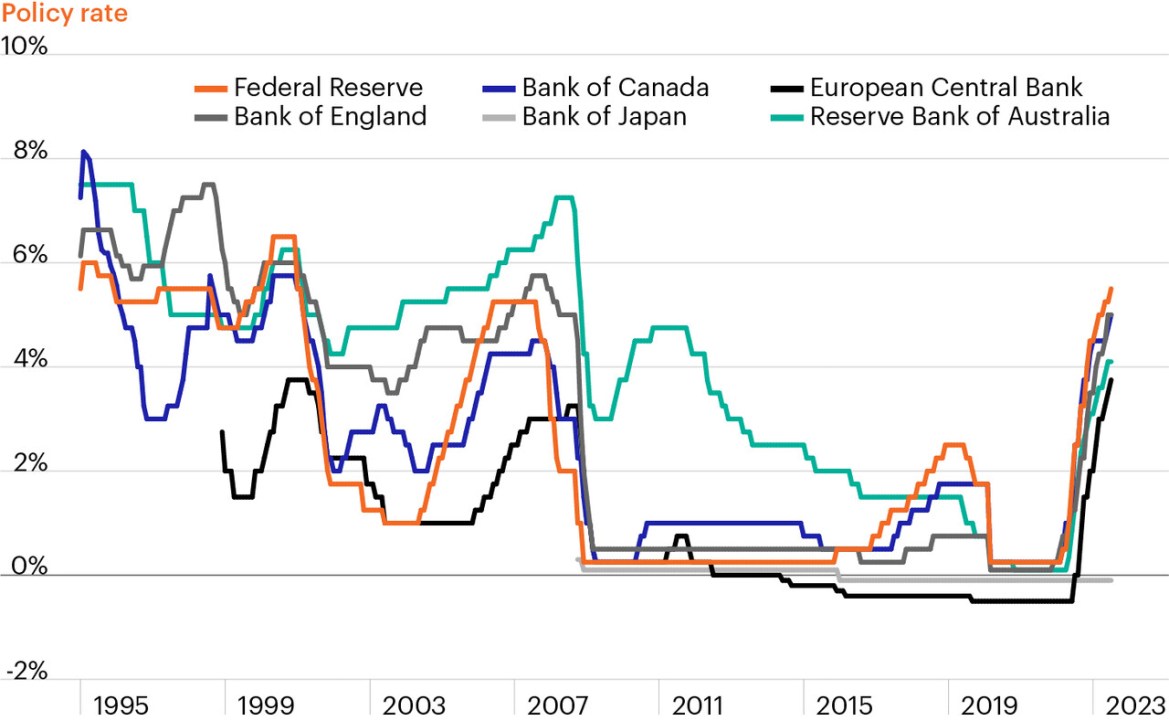

Chart 5: Major Central Bank Policy Rates until 2023

Japan:

Japan is the only country with a major central bank that is increasing interest rates, and the IMF is expecting the Bank of Japan’s policy rate to hit 1.5% by 2027 (a high rate considering the country’s history). On October 31st, the Bank of Japan decided to hold rates at 0.25%, opting to continue their rate hikes in December or January. After a snap election last week that produced no clear winners, the Yen has fallen relative to other major currencies. Across the Pacific, The Fed’s aggressive first rate cut has been seen by the world as a turning point for global markets, indicating the beginning of the Federal Reserve’s attempt at a soft landing. As the Federal Reserve tries to carefully steer the U.S. economy towards a safe low-interest environment, it is worth considering how the BoJ’s counter-cyclical (with regards to other central banks) policy and Japan’s changing market dynamics may affect American markets.

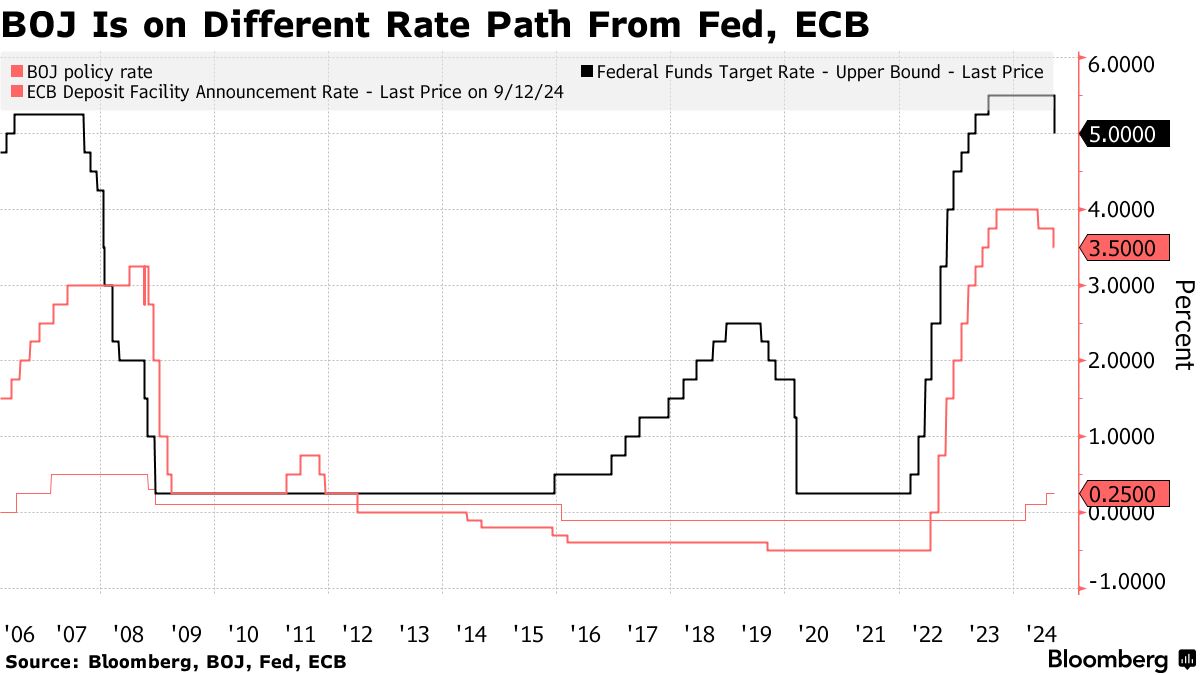

Chart 6: Bank of Japan Charts Different Course than the Fed, ECB

While Japanese policymakers are attempting to normalize their monetary policy (through rate hiking), Japanese Central Bankers are trying to do so without causing another early-August fiasco. In an effort to stop the deflation that has plagued their country since the 1990s, hiking rates in August has allowed the central bank to safely normalize monetary policy while carefully achieving their target inflation rate.

As the Fed cuts and the BoJ hikes, the dollar surprisingly continues to strengthen against the Yen, highlighting the strength of expectations of protective American foreign policy and Japan’s short-term political risks. The unpredictability of the first and third most traded currencies exchange rate over the past few months invites discussion over whether this trend will continue following Tuesday’s election. We believe so, as Japan’s domestic economy is still very much grasping for structural normality, and the Fed Funds rate cutting cycle is still very much not a clear path. In the case of a Trump victory, these effects would be more pronounced.

China:

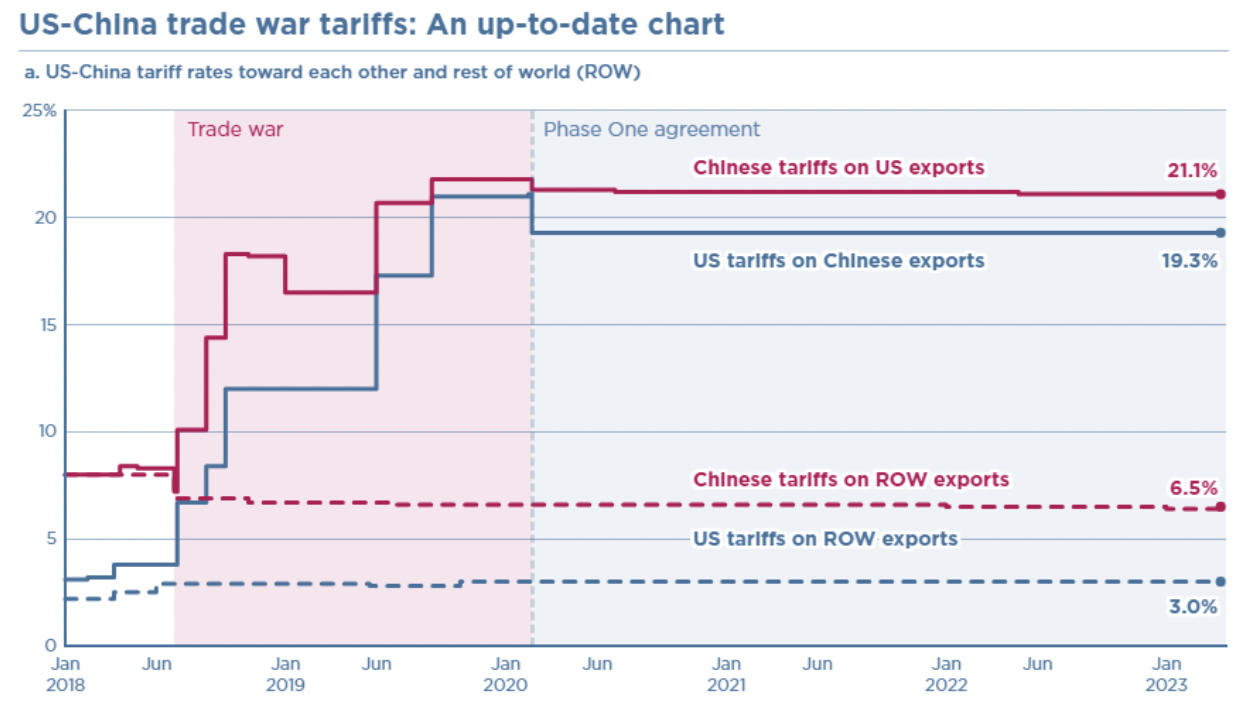

The effects of the U.S. election on China largely rests on tariffs. Throughout last week, as speculations of a Trump win grew worldwide, Chinese executives began to have conversations about what a Trump ‘tariff blitz’ would look like. Tariff blitzes’ are forms of protectionist trade policy in which import taxes on foreign goods rise very quickly or overnight. Regardless of the U.S. President-elect, the U.S. is poised to continue its trade war with China. The difference between the candidates is their aggressiveness. In 2018, then-President Trump imposed a series of duties on a variety of imports from China, effectively beginning the trade war. These tariffs totaled over $80 billion, levying tariffs against $380 billion of products from 2018-2019. The Biden Administration continued this Trump policy in September, adding an extra $18 billion in tariffs on Chinese goods, specifically targeting imports of electric vehicle parts.

It’s clear that tariff impositions cross-cut the political aisle due to the geopolitical competition between the U.S. and China, however, a Trump 2024 victory could mean a massive increase in tariffs and a changing global economic composition. The former President has proposed a 60% tariff on imported goods from China, and a 20% increase on imported goods from other countries. Brookings Institute economist Robin Brooks predicts that this could lead to a revitalization of the trade war between the U.S. and China, and the value of the dollar would rise “unlike anything in the past”. While this statement is bold with regards to the strength of the dollar, it highlights how unpredictable the balance of trade in the two largest economies may become in the event of trade war escalation.

Chart 7: Timeline of US-China Trade War

Europe:

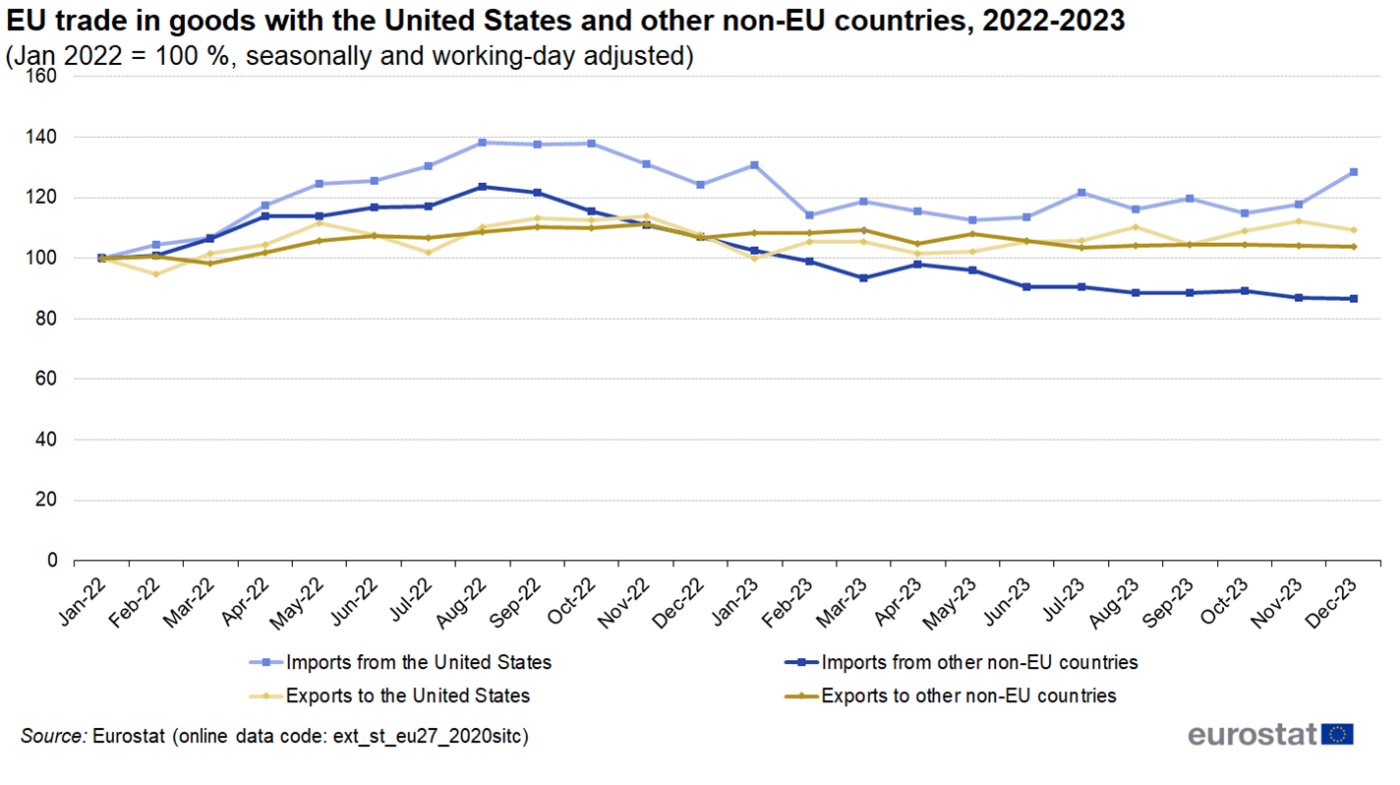

The European Union’s two largest trade partners are the United States and China and European officials are practically at the edge of their seats to see the U.S. election results. Europe is experiencing weak economic fundamentals and is desperately in need of some sort of stimulus (as argued on September 15th’s Weekly BluRB) amid their continued tensions with Russia. The results of the presidential election will provide hints to EU officials about their future course of action with a Harris victory seen by some as the “best” of two bad outcomes. Experts believe “Biden Continuity” through the Harris administration would facilitate trade relationships, positive diplomatic relations, and regional security, yet they would still not receive many favors.

Chart 8: EU’s trade in goods with the U.S. and other trading partners

However, a Trump victory has the potential to spark a geopolitical domino effect. If the U.S. pulls its support from Ukraine, which Trump has claimed his administration will pursue, the EU would rapidly need to increase its defense spending if they aim to protect Ukraine and their own border. This would likely cause Europe’s manufacturing economy to expand and transition into less of an export-heavy economy and more into a regionally connected network, whose strength depended on how active they were in Ukraine.

Seeing as Europe’s economy is already under duress, these structural concerns would be additionally exacerbated by Trump’s proposed 20% universal tariff on imports which has the potential to harm European export-led sectors. Furthermore, increases in tariffs on China would also bode poorly for Europe, seeing as export restrictions to China may be in order. The big loser from this election will probably end up being Europe, seeing as a changing world order seems likely to leave them out of the market if no internal changes are made.