It’s Parent’s Weekend, and Everyone Deserves a Break from Thinking About the Economy

Author: Andres Larios

Editors: Venus Dhanda, Sydney Sibrian, Daniel Hou, Faith Spalding

Intro:

Welcome to the Weekly BluRB, a newsletter catered to students and professionals to get the latest news and insights on global markets. Get prepared for the week by reading four weekly stories circulating around equity markets, macro trends, geopolitics, and new business developments. And the best part: we’ll give you an informed view about where we think prices, policy, and trends are going in the near future. The content in these writings is for informational purposes only and does not constitute financial or investing advice.

Last Week’s Calls:

Buy Financial Stocks: Goldman Sachs up 2.11%, Morgan Stanley up 8.95%

Fed 25 bp cut: 94% chance at time of publishing

Skeptical on Chinese Markets: SSE Composite Index up 0.69%, All other indexes in similar range

Equity Markets: No Story, Financial Stocks Perform (Really) Well

US Macro: The Fed Struggles to Read the Economy, and Traders are Profiting.

“Most recently, we have seen upward revisions to GDI, an increase in job vacancies, high GDP growth forecasts, a strong jobs report and a hotter than expected CPI report. This data is signaling that the economy may not be slowing as much as desired. While we do not want to overreact to this data or look through it, I view the totality of the data as saying monetary policy should proceed with more caution on the pace of rate cuts than was needed at the September meeting.” – Governor Christopher J. Waller stated on October 14th.

The economic outlook is uncertain, yet we can be somewhat certain we’re heading towards a soft landing. Governor Waller’s statement eyes for caution and perhaps alludes to the point that the data-dependent Federal Reserve didn’t act too data dependent once jobs data started cooling. Throughout the year before the Fed decided to cut rates, inflation data was priority number one. Starting in August, Chair Powell started referring back to the famous dual mandate in terms of how monetary policy will be enacted. This means, the plan was for the economists at the Fed to somewhat equally balance the priorities of stable prices and strong employment and economic growth when anticipating and acting on the rate cutting cycle. When shaky jobs data started to be released in August, our 25 basis point call seemed in line with supporting economic growth while not declaring victory over inflation… but we’re not here to complain.

The effect of this 50 basis point cut has seemed positive overall, especially after big financial institutions released strong earnings that beat analyst’s expectations. To Governor Waller’s point, the economy might be too strong, even with interest rates at 4.83%. While markets are pricing in a 94% chance of a 25 basis point cut in early November, in line with our house call, at the same rate, expectations of higher inflation are driving the back-end of the curve higher.

Chart 1: 10-Year Treasury Yield Throughout 2024

Chart 1 shows how after the 50 basis point cut in September, the ten-year’s yield has increased by roughly 40 basis points. While this highlights a dis-inversion of the yield curve, it also highlights the inflation risk of cutting aggressively. Thus, a sharp selloff following the rate cut news ensued, driving prices down and increasing the existing bond’s yield (not coupon). From a trader’s perspective, they bought the rumor (50 basis point cut impacting the front-end of the curve) and sold the news (inflation risk in the back-end of the curve).

Global Macro: Updates on China; Optimism in England, Rate Cuts in EU

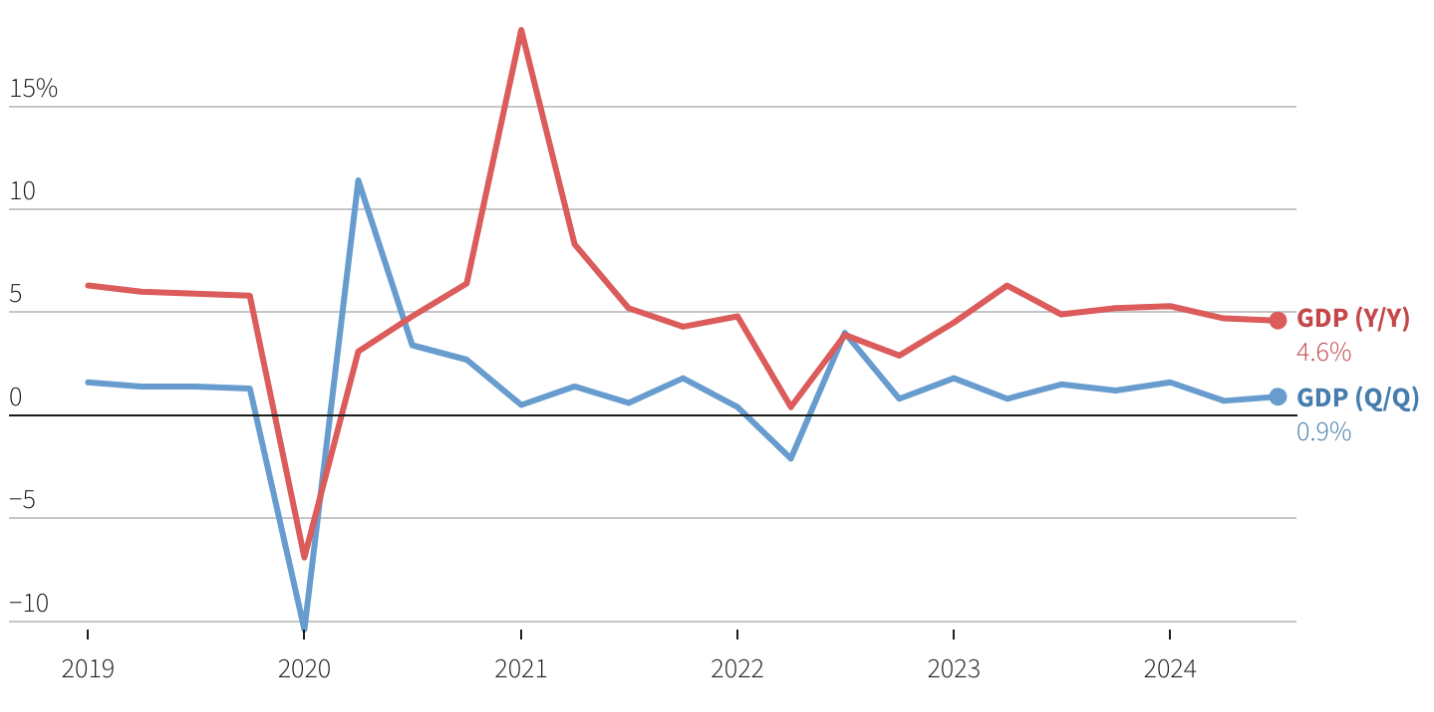

After last week’s section on China, we were looking forward to more clarity on the size of the stimulus package proposed by top economic officials. Unfortunately, we don’t have much more clarity on the size of the deal, but we now have a clear piece of data showing just how dire the situation is getting. This past week, quarterly economic data was released, showing the economy grew 4.6% in the last year (3Q-2023 to 3Q-2024), down 1% from the previous quarter’s reading. Seeing as Chinese economic officials target a 5.0% growth rate, these numbers are disappointing, scary, and highlight how China must stop notional monetary policy measures and begin implementing structural changes to get back on track. Investors are still unhappy with the economic plans proposed.

In lieu of this news, the People’s Bank of China (PBOC) triggered another set of monetary loosening policies including injecting 800 billion Yuan ($112 billion) into the country’s stock market on Friday. Furthermore, PBOC Chief, Pan Gongsheng, also signaled further key rate cuts. This bumped up Hong Kong’s Hang Seng Index at the end of the week by 3.6%, but raises questions about the sustainability of this market rally.

Figure 2: Year over Year and Quarterly Chinese Economic Growth

In the United Kingdom, last weekend’s International Investment Summit proved to be a success with £63 billion pledged by the end of the summit. These investments are estimated to create 38,000 jobs across the United Kingdom. The focus of the summit was investing in AI and data center infrastructure, with further pledges going towards achieving a net zero emissions economy.

Across the British Channel, the ECB met on Thursday, agreeing to cut interest rates for a third time this cycle, from 3.5% to 3.25%. This comes along with further data that the EU economy is weakening, however, ECB President Lagarde is still confident that the EU is approaching a soft landing.

Make sure to tune in next week for more market updates and global insights!