What’s Scarier: Being a Cal Football Fan with a 25 Point Lead or Skyrocketing Oil Prices?

Authors: Andres Larios

Story of the Week: Faith Spalding

Editors: Venus Dhanda, Sydney Sibrian, Daniel Hou, Faith Spalding

Intro:

Welcome to the Weekly BluRB, a newsletter catered to students and professionals to get the latest news and insights on global markets. Get prepared for the week by reading four weekly stories circulating around equity markets, macro trends, geopolitics, and new business developments. And the best part: we’ll give you an informed view about where we think prices, policy, and trends are going in the near future. The content in these writings is for informational purposes only and does not constitute financial or investing advice.

Last Week’s Calls:

Sell US Auto Stock – Rivian down 8.18%, Ford, GM stock rose with employment data on Friday

Fed 25 bp cut – 31 days to go

Oil Futures $70 LR Average – Check our Global Macro Section

Equity Markets: What Is Warren Buffett Plotting?

Following a strong employment report from the Bureau of Labor Statistics last Friday, the US stock market finished the week strong with the Dow Jones Industrial Average reaching a new record high price. However, despite the market’s strong finish, the week was characterized by instability, driven by various factors (detailed further in subsequent sections). Ultimately, the stock market doesn’t look like it’s slowing down, and as more data supportive of this notion trickles in, it is expected that these index valuations will continue to move steadily upward. September’s Consumer Price Index (CPI) print is set to be released on October 10th, offering investors another gauge of current economic strength and potential future shifts in Federal Reserve Policy.

However, despite bullish sentiment among equity traders who are pushing equity indexes to record highs, one Wall Street legend is shifting strategy–quietly offloading stocks, and reallocating to short-term treasuries and cash options. Warren Buffett, arguably the most famous value investor of all time, has expressed his desire for Berkshire Hathaway’s portfolio to consist of 100% stocks. As of now, the company holds a $313 billion position in company shares, and a $277 billion in cash and short term treasuries, meaning that, to Buffett’s disappointment, 46.9% of their active fund is now outside of business holdings.

Buffett’s new tactic began in early August when Berkshire Hathaway offloaded half of their shares in Apple and has continued after their recent unloading of $10 billion shares of Bank of America. These two stocks are the first and third most heavily weighted names in Berkshire Hathaway’s portfolio, respectively, leading analysts to question: What does he know that we don’t?

Buffett is known for seeking high long-term returns through fundamental investments, so his recent cash stockpiling suggests he anticipates a market pull-back or a drop in the valuations of publicly traded companies. By holding large cash reserves, Buffett is likely positioning himself to buy quality stocks at lower, more attractive prices once the market adjusts.

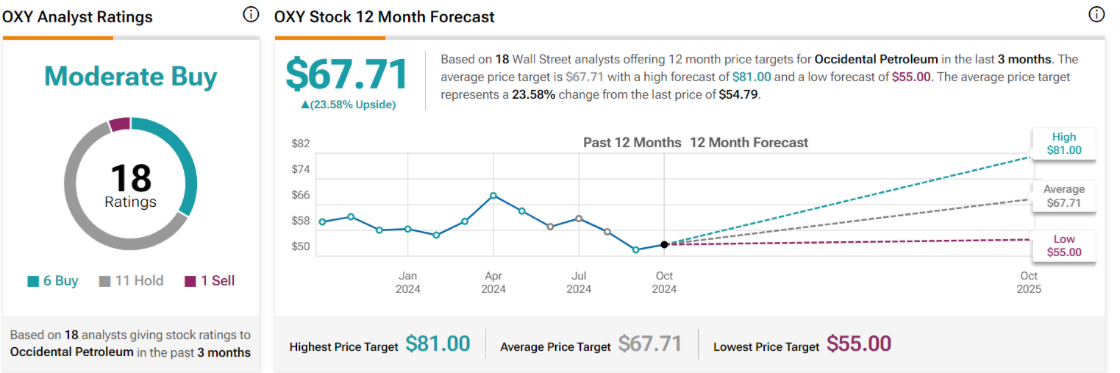

But what is the Oracle of Omaha now buying? Occidental Petroleum, an American oil-producing heavyweight, is poised to grow in a lower interest rate market and despite rising geopolitical complexities surrounding oil. Mirroring Buffet’s strategies in stock selection often proves wise for investors, and besides its strong fundamentals, Occidental Petroleum is especially insulated from oil conflict zones in Eastern Europe and the Middle East. The stock’s price has increased by 8.76% in the past five business days, and we expect it to continue rising regardless of increasing tensions in the Middle East (read more about the Middle East in our Global Macro section).

Chart 1: OXY Stock Wall Street Analysts 12 Month Forecast

{kind=link}

US Macro: Despite Noise, The US Economy Is Strong (Right Now)

A lot of news came out this past week, including a short-lived strike involving 45,000 dockworkers, really strong labor data on Friday, and of course, a thrilling Vice Presidential debate! What does this all mean for the economy? It means, despite a lot of noise, the US economy seems to be moving along in the right direction. Let’s get into the highlights of the week.

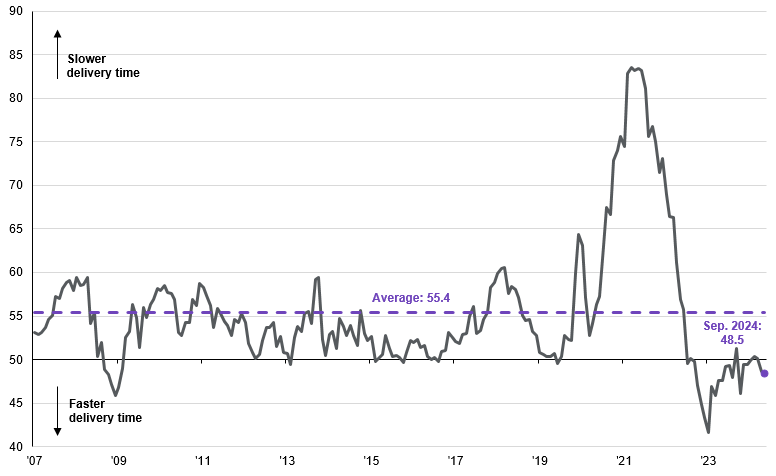

On October 1st, dockworkers on the East and Gulf coasts went on strike due to growing fears of automated technology replacing their jobs. These fears are not unfounded as physically intensive labor practices are becoming increasingly outsourced to automated machines that require minimal oversight. Thus, the International Longshoremen’s Association (ISA) sent ripple waves across the United States as top research firms predicted the US economy could lose anywhere from $4.5-7.5 billion for every week of the strike, showing how important labor still is. The strike negatively affected roughly 36 ports as 45,000 ISA members advocated for a 77% wage hike. Instead, the ISA and their employers, represented by the United States Maritime Alliance (USMX), unofficially agreed to a 62% wage increase over six years, ending the strike on Thursday night. According to JP Morgan Asset Management, the United States’ supply chain was well positioned for such a strike (Chart 1), meaning that although the three day strike was disruptive and caused backlogs, the return to work on Monday should be seamless.

Chart 2: US Supply Chain Delivery Time Below Historical Averages

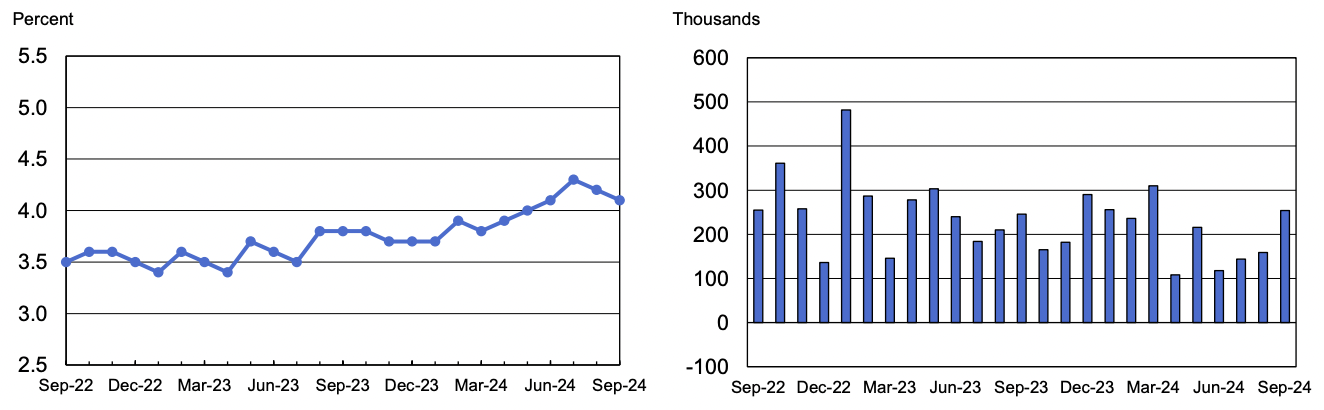

Speaking of how strong the US economy seems to be, how about Friday’s Bureau of Labor Statistics report? The report, released Friday morning, showed that the US economy added 254,000 jobs in September, beating Wall Street analysts’ expectations, causing the S&P 500 to rise 0.90% and the Russell 2000 to rise 1.50% on Friday. Furthermore, Wall Street is now pricing in a 97.5% chance of a 25 bp cut in November, in line with our forecast. An important note from this report was its consideration of the effects of Hurricane Francine towards measuring the jobs data, finding no discernible effect in short term employment numbers. With Hurricane Helene hitting the Southeast this past week, it is becoming increasingly important to account for climate disasters when measuring the current state of the economy.

Chart 3: Nonfarm Payroll Unemployment Rate and Monthly Employment Change

In spite of this past week’s labor strikes, good jobs data, and a tariff battle with China looming over the United States’, it remains important to look into the future by analyzing proposed policies in this past Tuesday’s Vice Presidential debate, a conversation regarding women’s health, gun rights, and of course, the economy:

Exclusive Story of the Week: Economic Takeaways From a Civil Vice Presidential Debate

Tuesday’s Vice Presidential debate was one where civility prevailed, a favorable departure from disparaging partisan dialogue that has headlined the past several election cycles and divided the nation. However, just as Former President Trump’s crass debate rhetoric is expected, so is Vice Presidential candidate Governor Tim Walz’s (D–Minn.) “nice-guy” persona. By Walz refraining from more direct, aggressive attacks on GOP racial insensitivity, abortion restrictions and immigration, Senator J.D Vance’s (R–Ohio) surprising agreeability may be perceived as a refreshing GOP debate advantage. Many of the issues on American voters’ minds centered on economic policy, seeing as it wasn’t discussed in detail during the Presidential debate.

Walz targeted middle-class voters, emphasizing Vice President Harris’s plan to direct billions of federal dollars towards manufacturing, increasing the number of houses and downpayment assistance, and renewed child tax credits. Walz’s reminder of the 8% increase ($8.4 billion) in national debt due to Trump’s 2017 tax reform plan was a strong counter to Vance’s sharp criticisms of Harris’ seemingly costly plan.

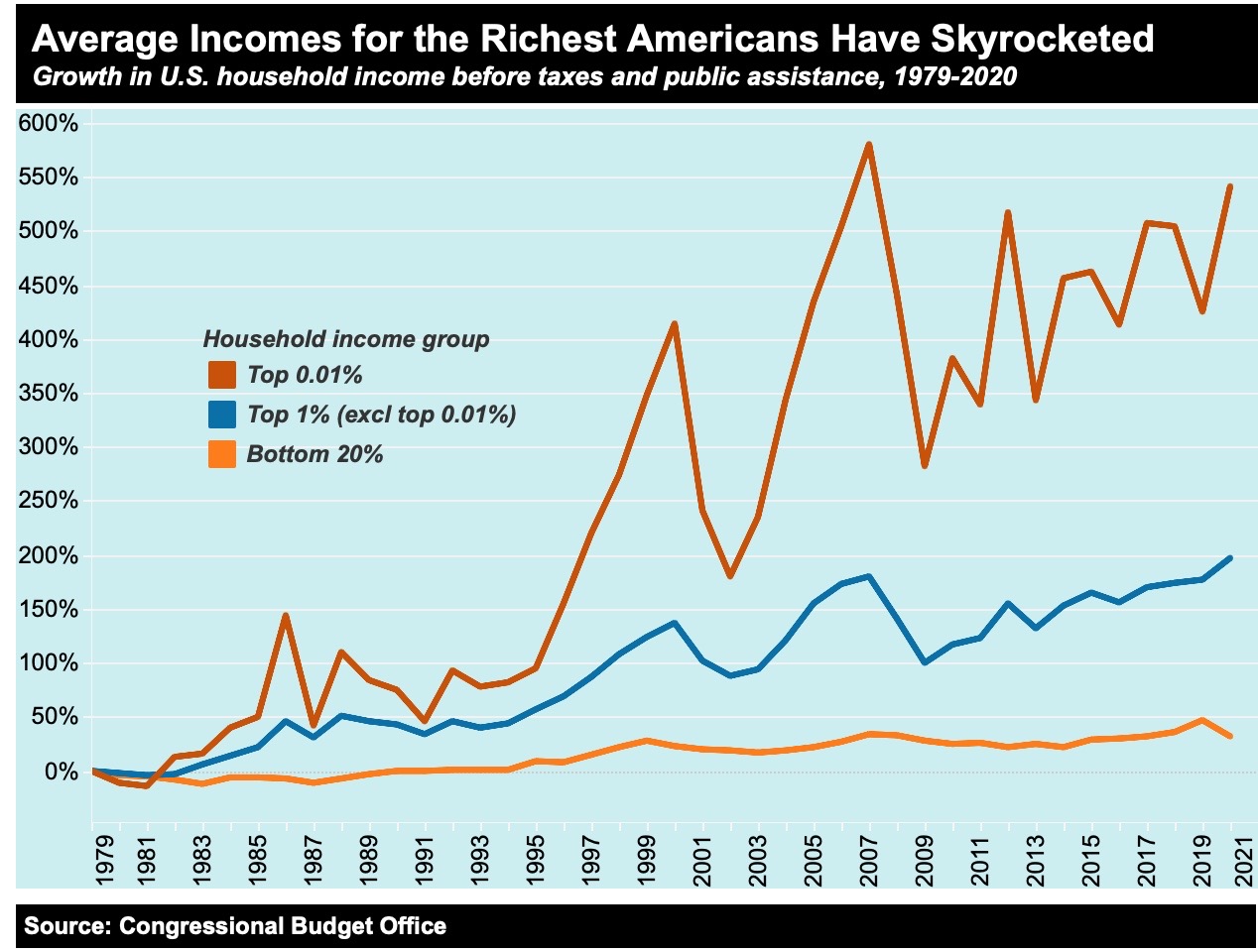

While Vance’s initial comments blamed Harris’ current executive inaction on high inflation and cost of living, he emphasized the high take-home pay and low inflation rates reported under Trump. In particular, he noted that Trump’s 2017 tax cuts catered to the middle-class, but Vance’s claims that Trump’s 2017 tax cuts directly aided the middle class were false. In fact, they favored the wealthy by slashing tax rates for corporations and the top 1% of earners. A study from the Center for American Progress analyzing past Trump tax policy reveals that as a result of these cuts, middle class households in 2025 will receive an average tax reduction of $910, whereas those in the top 1 and 0.1 percent will receive payoffs of $61,090 and $252,300 respectively.

Chart 4: Income Inequality Skyrockets Since 1980s

It’s clear that these benefits have not “trickled down” into major tax improvements for the middle class. With estimations that Trump’s plan will increase the national deficit by $5.5 trillion and Harris’s by $1.2 trillion, there remains no explanation from either candidate as to how to prevent the budget deficit from ballooning, which could potentially lead the country into a recession. When discussing additional reform plans for affordable housing during the debate, Vance pursued claims that undocumented individuals in the U.S. are driving up housing prices for the average American, whereas Walz blamed Wall Street for treating housing as “a commodity,” defending Harris’s $25,000 down payment assistance plan for first-time homebuyers.

Chart 4: Income Inequality Skyrockets Since 1980s

We’ve discussed important economic takeaways from the debate, largely centered around housing, tax cuts and their impact on the middle class. But beyond the fiscal focus, both candidates presented targeted policy proposals on a myriad of issues. Vance’s energy at the end of the debate was rabble rousing as he refused to definitively say that Trump lost the election in 2020, but his final answers were concise attacks on Harris’ (lack of) policies, highlighting that the “American Dream” has been diminished under broken leadership. Walz, on the other hand, emphasized a sense of optimism that an opportunity-economy under a Harris administration would allow Americans to “get ahead.” What is abundantly clear is that this debate was incredibly Midwestern, defined by Walz’s expected civility and Vance’s attempts to reframe Trumpism in a reasonable light.

Global Macro: At This Point, Should We Just Call This Section Global Oil?

Yes, we’re talking about oil again. But know that when we talk about oil, it’s for a good reason! Besides, about 40% of the world’s energy comes from oil, it’s the world’s most traded good, and countries go to war for oil rich territories. This past week demonstrated how important geopolitics and conflict are for the price of a single barrel of oil.

Last week, we forecasted a $70 long run average price for oil futures. Our call was looking reasonable until Iran launched a ballistic missile attack on Israel last Tuesday, in response to Israel’s devastating strikes on Lebanon. Although Israel’s infamous Iron Dome prevented any major damage from the approximately 200 missiles launched at Tel Aviv and targeted military bases, Israeli President Netanyahu’s immediate response was that Iran “made a big mistake”. It is reported that the IDF is planning a deadly response against Tehran. Unsurprisingly, fears of an all-out armed conflict in the world’s most oil-rich region drove up the price of oil to around $75 a barrel at the end of the week.

There is also the additional threat that both sides of the conflict will begin to start targeting energy infrastructure. Iran, the third largest oil producer in the Organization of the Petroleum Exporting Countries (OPEC+), exports most of their oil from a terminal on Kharg Island, which is 25 km off their southern coast. After Israeli officials stated that they could hit any part of the Middle East, geopolitical fears have global leaders shaken. Ben Luckock, Global Head of Oil at Trafigura (the third largest commodity trading firm) stated, “Where the price goes from here will be determined by what Israel specifically targets within Iran. We are all watching and waiting.” On Thursday, President Biden stated with regards to Israel’s possible response, “If I were in their shoes, I’d be thinking about other alternatives than striking oilfields.”

Chart 6: Post-Pandemic Oil Prices Characterized as Volatile

This talk shows the global importance of a stable oil supply. During the beginning of the Russia-Ukraine war, oil prices peaked at $130. A prolonged conflict in the Middle East could drive prices back to that range, especially if key infrastructure is targeted, or if Iran decided to impose themselves in the Strait of Hormuz. A blockade on the Strait of Hormuz would be catastrophic for oil supply, natural gas supply, and global trade as a whole, as well as increasing the probability of a large-scale energy war.

For the past few months, traders and analysts have worried about softening demand curtailing the price of oil, but now that the regional risks are right in front of us and the US and China are both stimulating their economies, we should begin to look again at how major oil nations are shifting their production, allocation, and regional pricing for energy commodities.

Make sure to tune in next week for more market updates and global insights!